Monthly commentary

Summary

At the end of last year, the vast majority of economic and market forecasts were really negative, and, to a large extent, they still are. So, why is everything rallying and does that mean it’s going to be plain sailing for markets for the rest of 2023?

First, here’s what happened in equity markets in January:

| Index | Jan 2023 Price Return |

|---|---|

| S&P 500 | 6.2% |

| Nasdaq | 10.7% |

| FTSE 100 | 4.3% |

| TOPIX | 4.4% |

| MSCI EM | 7.9% |

| EuroStoxx 50 | 9.8% |

As you probably know, we are underweight equities at the moment. So, it should come as no surprise that we don’t think equities will continue this stellar rally. Here are a few of the possible reasons why the tick up in equities has happened, and more importantly, why each one isn’t the sign we are looking for to bring our equity allocation back up to neutral:

- Premature pivot narrative. There has been a lot of optimism around US inflation data getting slightly better. The US inflation figure you tend to hear in the news (US year on year CPI) has fallen from 9.1% in the middle of last year to 6.5% at the start of this year. This is a good sign and it’s what is getting markets excited, but inflation is still a long way above its 2% (Personal Consumption Expenditures) target. Prices are STILL increasing at 6.5% per year!

The Fed will want to have inflation dead and buried before they pivot. Jay Powell will want to be remembered as a Fed Chair who slayed the inflation beast in one go, and not one who pivoted prematurely and got bitten again. We still have some way to go until the Fed actually change their tune – but the market refuses to believe it.

- China… Licking your elbow is really hard, but predicting what will happen in Chinese policy is even harder. After three years of President Xi’s zero Covid policy, China is reopening both internally, and to the rest of the world. This has caused a lot of excitement around Chinese equities and hard commodities.

A continued reopening would have a big positive impact on global demand, but there is a huge amount of uncertainty. Would a demand boom from China cause inflation? Will Xi lockdown again when hospitals become overwhelmed? Could Xi attack another sector as he did with real estate or education? All of these are tough to predict, and excitement around China could be misplaced.

- Europe is getting some good news. A big concern for Europe since February 2022 has been natural gas prices. Over the past couple of months, these have returned to pre-Russia/Ukraine invasion levels, giving Europe’s inflation and the European consumer some respite. Other factors such as the Purchasing Managers’ Index stabilization, slightly better earnings revision trends, and hopes of a demand boost from a China reopening have also contributed to positive sentiment.

These are definitely good signs, but they are not the foundations for a global recovery. Europe does not drive the global economy, and bad weather could derail a lot of the good signs Europe is seeing anyway.

- Bear market rallies do just happen. You might remember, I wrote about a few examples of bear market rallies back in November. The majority of bear markets experience some sort of bear market rally. They can be fast, slow, deep, shallow, completely unexpected, and painfully recurring. One example of a bear market that experienced pretty much all of this was the 2000-2001 dot.com crash. Over this period, the Nasdaq entered eight bear market rallies greater than 18%, none of which materialized into a bull market.

In short, expect some bear market rallies. They don’t necessarily mark the end of tougher times.

Actions taken

During January, we have:

- Slightly reduced our alternatives overweight in favour of fixed income. Our alternatives basket has performed extremely well in stressed market conditions, but the base level of return for bonds is higher now, resulting in a higher hurdle to be as overweight alternatives as we were.

- Introduced a metals and mining trade. We have a lot of conviction in this trade as a long-term theme. The amount of metal needed to get to net zero is vast, and the nature of mining means that supply cannot increase in line with this. Mining companies are likely to benefit. Furthermore, the companies are cheap and produce very healthy dividends.

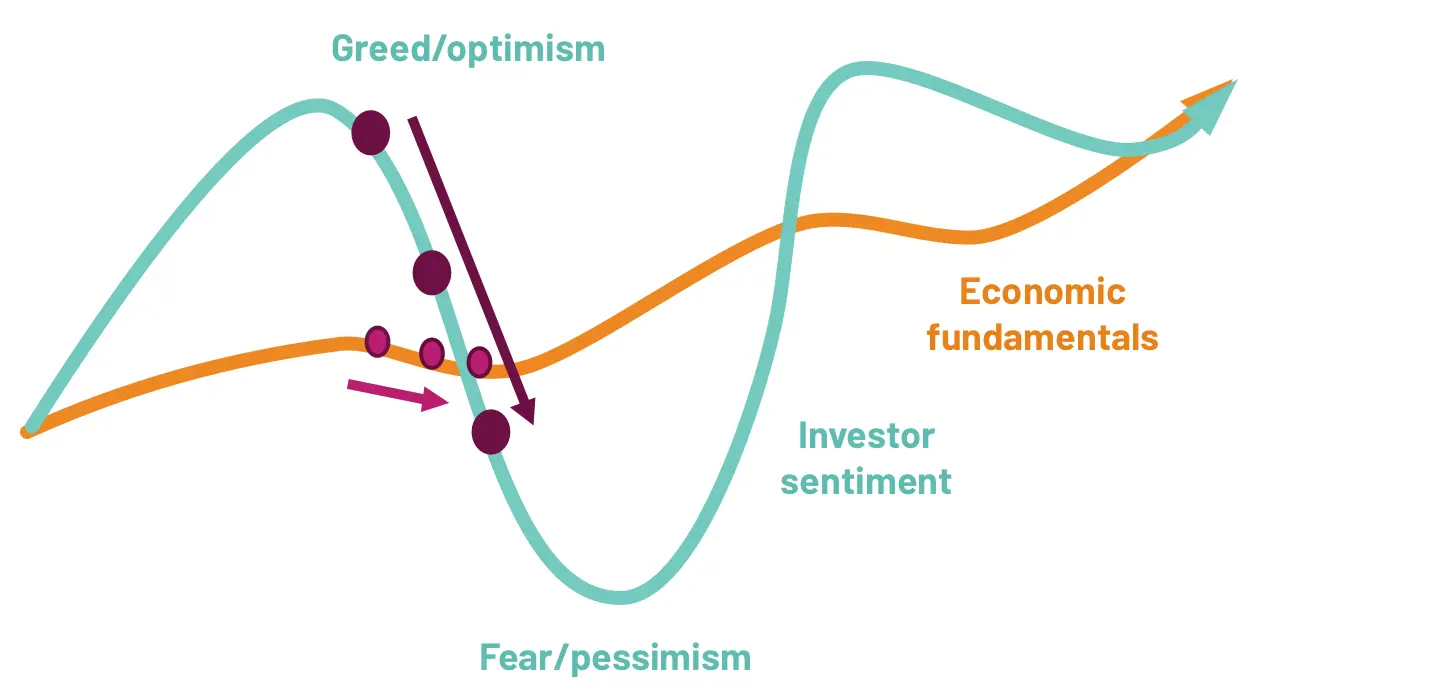

Investor sentiment overreacts to economic turning points …

… with slightly weaker data leading to panic right now

Source: 7IM

Core views

At 7IM, we have a number of long-term core views that help to guide our investment decisions and allocations within portfolios.

Over the next twelve months, we think markets will generally move sideways with volatility. In this environment, it is important to rely on a stable identity. Economic uncertainty creates fear and investor sentiment tends to overreact to economic turning points. Going forward, we believe that:

- Inflation will come down. Goods inflation is slowly normalising, and supply chain pressures are easing.

- Central banks are getting close to the end of their hiking cycles, but there is still a bit more work to do.

- A US recession is highly likely. Most leading indicators point towards a recession, but the recession shouldn’t be too long or deep.

And so, investors are starting to worry about what’s next for financial markets. Economic data isn’t likely to stabilise until next year, so ‘Sideways with volatility’ is the most likely scenario for the next few months.

We know our investment identity helps us to deliver in just these kinds of environments. We have positions that can generate returns despite this volatile backdrop.

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.