Monthly commentary

To the moon? Or failure to launch?

"How do you make a small fortune in the airline business?

… Start with a large one."

It's an old joke, but it's true: airlines are a seriously tough business to make money in. Profit margins are tiny, competition is fierce, planes are capital-intensive, and you're exposed to volatile fuel prices and a unionised labour force. And of course, you’re only ever one accident away from reputational disaster.

Is the same true of rocket companies? Up until this month, we’ve never had to find out. Space travel has been the preserve of governments and billionaire pet projects.

SpaceX went public in the middle of June – the largest IPO (initial public offering) in history. But if you think airline profits are low, how about turning $20 billion in sales into a $4 billion loss? Analysts at research firm Morningstar opined that the IPO raised a "material threat of value destruction".

Of course, there is a bull case. SpaceX's technical accomplishments are miraculous. It owns a profitable satellite internet company which is growing at 70% annually. It is also plugged into valuable government contracts and counts Alphabet and other Artificial Intelligence (AI) giants as customers. But is that enough to justify a ~$2 trillion market cap, making it the sixth largest business in America?!

The IPO has got to go down as an early success. The shares traded up to $165 from the original price of $135, and after some initial shenanigans, that’s roughly where they’ve stayed. The market seems to believe.

But SpaceX is just the most recent example of the headaches big companies can cause for stock pickers. You can’t credibly put SpaceX into a carefully constructed portfolio – any conventional analysis of profits and revenues allows it nowhere near, and there are no textbook metrics for “Elon Musk Magic”. But equally, what if it keeps going up? What if it is the best investment of the next decade? A number of managers ignored Tesla for similar reasons and suffered underperformance as a result.

Indices have been facing the same problem. The rise of passive investing was built on the back of the idea that stock picking is very difficult, and often not worth the bother. And most of their rules don’t let newly listed companies join straight away. But at the same time, lots of their clients will say that they just want “all of the companies” and that it’s not an index provider’s place to pick and choose who makes it in… after all, isn’t stock picking meant to be difficult?

Still, there’s no escaping the fact that, at the moment, Elon Musk has a large fortune. The interesting thing is what happens next…

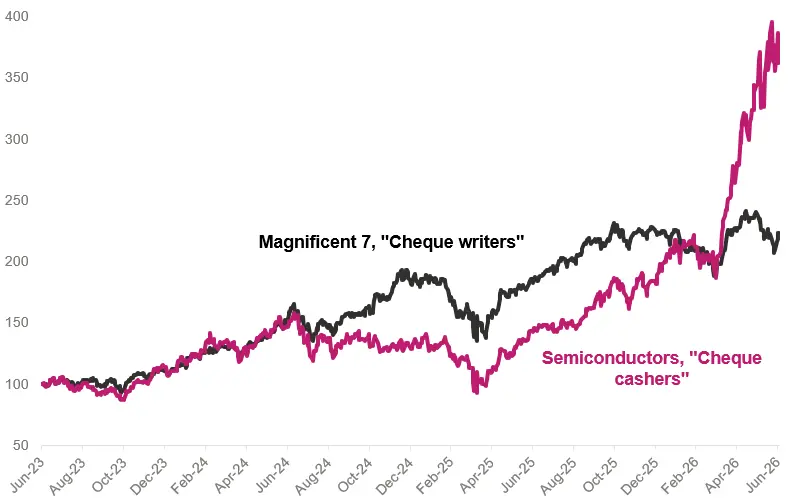

For a while, the market treated AI as one trade. If a company had some kind of exposure to AI, it went up. Everything was pulled into the narrative.

But over the last three months, investors have become more selective, starting to ask: "who actually reaps the economic benefits?"

The black line shows the cheque writers. Think: Alphabet, Microsoft, Oracle. They’re spending money on data centres, land, chips, and power.

The pink/purple line shows the cheque cashers. These are the companies making the semiconductors, memory, and storage – the physical stuff used to make AI work. These are companies like Nvidia, SanDisk and Micron.

The companies in the black line are sending money to companies in the pink line. The cheque cashers have the power, and that’s been reflected in their share prices.

We've seen divergences like this before, in other industries – railways, telecoms, shale – where the suppliers often did better than the spenders.

For the gap to close, big AI spenders will need to start showing that their outlays are increasing their profits, rather than just the profits of those they’re buying things from.

Source: FactSet: Roundhill Magnificent Seven ETF and iShares Semiconductor ETF, both in USD

June markets wrap

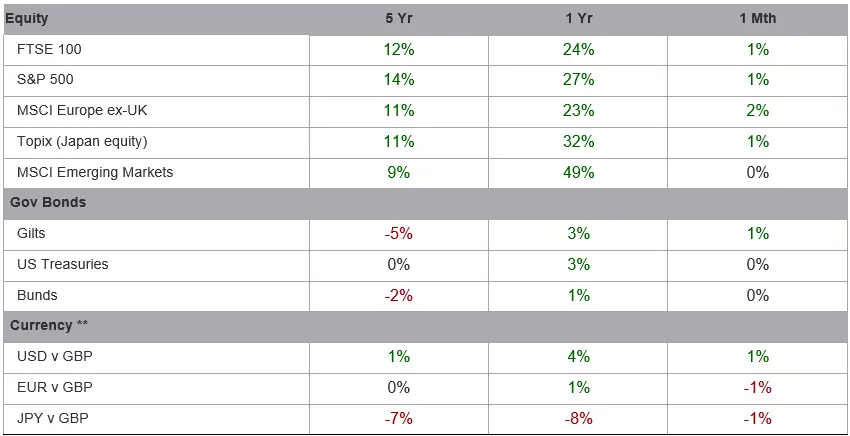

Headline figures for June were mildly positive, albeit volatile. Early in the month stocks tumbled on AI bubble fears but later rebounded as a patchy peace deal in the Middle East brought down borrowing costs.

AI stocks were trading wildly, as the market yo-yoed between euphoria and fear. The chipmaker Micron saw its stock drop 13% in a single day but later delivered a blockbuster earnings report and rebounded to record highs. We’ve also seen a growing gap between those companies spending on AI and those supplying the hardware – see chart of the month, above.

There was some variation by geography. The UK eked out a positive return, but the US struggled as some of the mega-cap names wilted. Apple, Alphabet and Microsoft all ended the month down double digits from their earlier highs. The stronger dollar helped prop up returns for sterling investors (see the table below), but the result was still essentially flat overall.

Europe was mixed, with France in the green but Germany in the red, after the Bundesbank said that the EU's largest economy would only avoid recession thanks to a spike in government spending.

Emerging markets were mostly negative, despite continued strong performance from South Korean chipmakers. Stock fell in China, adding to the gloom in the world's second largest economy, as data showed Chinese property prices continued their slump and hit a 20-year low.

Gilt yields inched down from 4.8% to 4.7%. Keir Starmer's resignation and the likely rise of Andy Burnham to the top job initially rattled bond markets, on fears of an unfunded fiscal splurge. But the former Manchester mayor moved to soothe investors by committing to the existing "fiscal rules" which limit borrowing.

Market movers

Quoted returns are in GBP

What we’re watching in July

9 July – deadline for Labour MPs to put themselves forward for the leadership race – will Andy Burnham be coronated, or will he have to fight?

22 July – UK CPI release will show if inflation has entered a self-reinforcing spiral or if lower oil prices are already cooling things down.

24 July – Trump's temporary tariffs expire, with new policies or an extension likely to be announced.

30 July – half-year results from Lloyds Bank, which should shed some light onto the state of the UK housing market and consumer confidence.

More from 7IM

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.