Drawdown for lower risk clients

2022 was not a good year for many multi-asset investors. Government bond indices experienced their worst drawdown since Napoleonic times, hitting those in lower-risk profiles especially hard. For investors at or near retirement, looking to turn savings into an income, portfolios falling in value may have been especially concerning. However, if the goal was to provide income, things may not be as bad as they first seem.

Annuities have been an unpopular retiree choice for some time. So-called ‘pension freedoms’ removed the obligation for many to buy an annuity back in 2015. Ever since, there has been a clear bias toward not ‘securing’ income and instead utilising a drawdown approach. Low bond yields meant the rates on offer from annuities simply weren’t attractive to many. However, that tide started to turn in 2022. Annuity rates hit a 14-year high, whilst annuity sales rose 13% in 2021/22, according to FCA data.

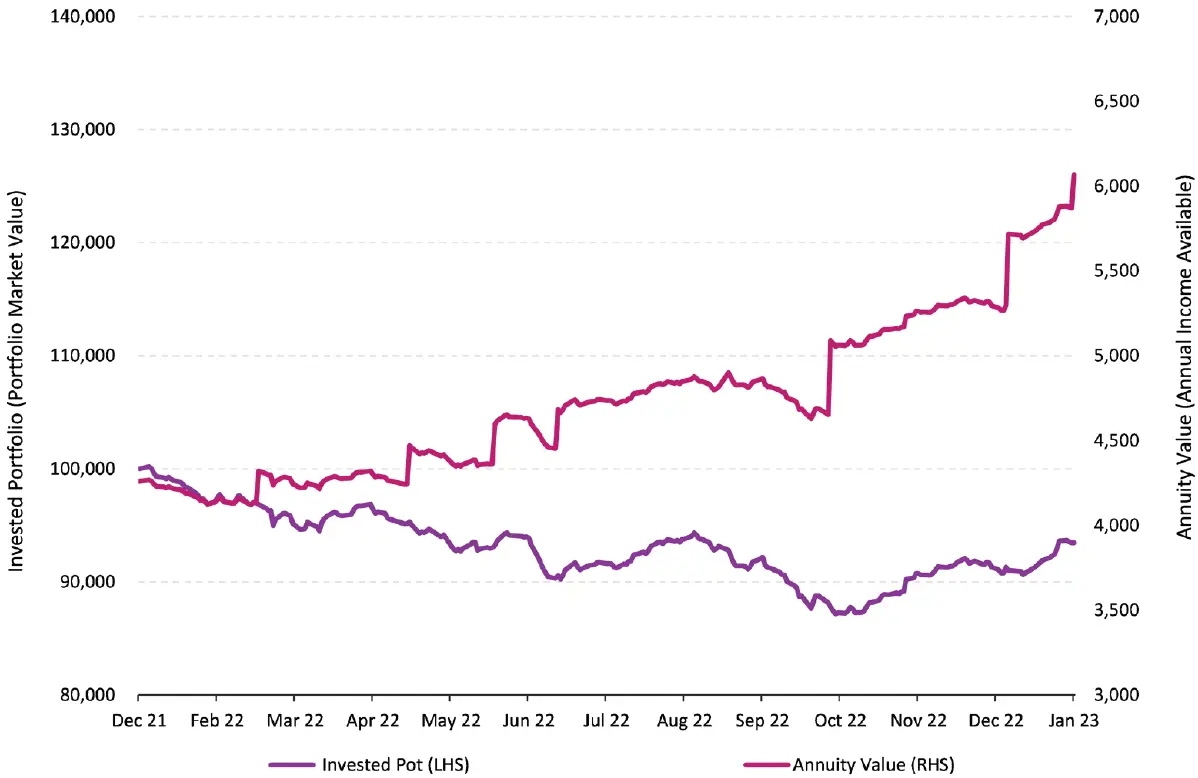

The power of the reset in annuity rates is clear from the chart below. It shows the performance of £100,000 invested in the AAP Moderately Cautious fund versus the value of the income that could be secured through time. The invested portfolios saw a drop in value through 2022, but the increase in annuity rates more than offsets this. Our investor with £100,000 could have purchased an annuity paying close to £4,250 per year at the start of 2022. By January 2023, they would have ‘only’ around £93,500 left to buy an annuity. However, they could use this to secure a significantly higher level of income, at closer to £6,100. Their portfolio had seen a drawdown, but in terms of income the picture at the end of the year looked significantly better than at the start!

Source: 7IM and JUST

(Based on average health, non smoker)

This is an important reminder of the power of framing when it comes to retirement planning. Portfolio market value is simply one component when assessing the ability to meet a retiree’s goals. In the case of a drawdown approach over the last year, any cash flow calculations should reflect the increased guideline returns associated with multi-asset portfolios today versus a year ago.

Higher yields on government bonds, higher cash rates and lower valuations for some ‘riskier’ assets are more of a tailwind going forward.

| Cautious | Moderately Cautious |

Balanced | Moderately Adventurous |

Adventurous | |

|---|---|---|---|---|---|

| Today | 4.8% | 5.3% | 5.8% | 6.1% | 6.4% |

| 2022 SAA | 4.3% | 4.8% | 5.4% | 5.9% | 6.2% |

| 2021 | 2.8% | 3.6% | 4.3% | 5.0% | 5.4% |

| 2020 | 2.9% | 3.6% | 4.4% | 5.0% | 5.5% |

Source: 7IM and JUST

(Based on average health, non smoker)

Portfolios invested for clients in or approaching retirement may have raised some angst in the last year, given market volatility and falling portfolio values. Despite the example discussed, for those who are younger, with higher risk appetites or larger retirement pots, the flexibility of a drawdown solution will likely still be the most attractive solution. For that cohort, the increase in portfolio expected returns likely means many plans remain more on track than headline falls in portfolio values would suggest. For those who are older, or those with a much lower risk appetite, the increase in annuity rates (or other ‘secured’ products, such as JUST retirement’s SLI product) may now be a compelling option. Centralised retirement propositions should aim to offer all of these approaches in a structured way. The benefit of getting that right is that despite recent volatility, most plans are probably more on track than most clients (and some advisors) realise!

You can download the article as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.