If I were an influencer

If you’re on the ‘socials’, your timeline will fill up with content you like. At least, it’ll fill up with content the algorithms think you like. Whether you’re into working out, cooking or trainspotting, there’ll always be a post ready for you. Different content providers and influencers will find ways to hook people into their channels.

An easy way to do this is to have a clickable title. Gym-goers won’t be interested in “How alcohol negatively impacts hypertrophy”. But “How drinking KILLS your gains!” will generate plenty of clicks.

Another way to do this is through a simple countdown: “Five things I wish I knew before I started the gym” or “The three most import kitchen items” or “Top 10 trains in Europe”.

It made me wonder: what if I were an investing influencer? What would be my hook? Well, with UK interest rates where they are, mine would be “Three BIG problems with cash”.

It’s crucial to remember that portfolio returns don’t happen in nice, neat segments but are unpredictable and lumpy. The risk of moving to cash is that you miss out on the big years."

1. The natural order of things is for cash to lose against every other investment

Multi-asset portfolios are made up from different asset classes. In the most traditional form, these tend to be government bonds, corporate bonds and equities. These aren’t just pieces of paper with a theoretical value, but rather one side of a mutually beneficial transaction. You, as an investor, are looking for a return on your money, while on the other side there is someone who needs that money and is willing to pay you for it!

And these companies and governments that need your money have to offer you more than a cash return … otherwise you’d just hold cash. And the return you get tends to line up with the risk you take – the less certain the outcome, the more you’ll want to tempt yourself away from cash. And this isn’t just theory (see Cash is the lowest common denominator section below).

The upshot is that those financial assets are designed to deliver returns higher than cash – that’s the minimum they have to deliver! This means multi-asset portfolios, by design, should also beat cash over the long run.

2. You give up predictability for higher returns

The comfort of cash is alluring. You know exactly the return you’ll get (sometimes to multiple decimal places), the journey that return will take and over what time. So, when interest rates are high (as they are now), it’s tempting to move long-term savings into cash. After all, what are the chances that a multi-asset portfolio is going to beat that over the next year or two? I mean, aren’t we headed for a recession anyway?

The problem is that asset class returns are unpredictable. Take US equities: on average, equities are supposed to deliver around 10% a year. But how many of the last 50 years have the returns of US equities actually been 10% (or say 2% either side)? The answer is three. Just three!

Most people think that, when cash rates are high (say today’s 5%), they are willing to give up the rule of thumb 10% return from equities – it’s not that big a difference and it’s only for a year or two. But what if I said that nearly a quarter of the last 50 years have seen returns of 20% or more? Moving to cash risks missing out on these returns.

It’s crucial to remember that portfolio returns don’t happen in nice, neat segments but are unpredictable and lumpy. The risk of moving to cash is that you miss out on the big years. Those big years make up for the smaller years. Therefore, missing out on those will impact your overall long-term returns. The problem is, it’s difficult to know when those big years are likely to be.

The key is to stick to your investment plan, even when uncertainty is high. Strong years will often follow the worst ones, meaning over the long run your portfolio should beat cash.

3. Your biases can be to the detriment of your long-term returns

With all the negative headlines out there – Russia this, AI that, inflation the other – it feels like a poor environment for investors to make returns. ‘I’ll just park into cash for this year, see out the storm and then invest when things look a little rosier’. Let’s play out a couple of thought experiments:

Scenario 1 – markets down, cash wins. Most investors imagine in that scenario they will act rationally – “markets are down, they look more attractive, I was right, but I won’t ride my luck anymore, so let’s move cash back into the markets”. The truth is this is very rarely how it plays out. Most investors tend to be led by markets. If markets are falling, it means uncertainty is high and they tend to be followed by scary “$X billion has been wiped off the stock market” headlines. The result is that investors sit out for a while longer, missing out on the recovery, often to the detriment of their long-term savings goals.

Scenario 2 – markets up, cash loses. Most investors imagine in this scenario they will act graciously, accept defeat and move back to investing, chalking it up to one bad call. Instead, investors will tend to see markets up, climbing the so-called ‘wall of worry’, against their own expectations. When one gets a call wrong, it is tempting to believe it’s the market that’s actually wrong – perhaps it’s got ahead of itself, so let’s sit out a while longer. The result is missing out on new highs, often to the detriment of their long-term savings goals.

These sound like theoretical scenarios, but they are outcomes of long-term studies. One of the longest running of these is the Dalbar QAIB1 survey. The report looks at the average US investor returns compared to if they had just invested passively in the index of large US companies.

The study found that since 1992 investors on average earned 3.5% per year less than if they had just left their money untouched.

Investors often change their investment plans, not based on their goals but on current market and news. And the impact is huge! These changes – whether into cash or into a new manager or a new style – are often… you guessed it… to the detriment of their long-term savings goals.

Away from social media

Putting it all together, moving a long-term investment pot to cash isn’t wise. But that’s not clickbait; we’re not saying something controversial just to make a splash. It’s the right way to think about things – and at 7IM we do exactly that, regardless of whether it gets us any attention.

A typical 7IM Cautious portfolio will have around half of it lending to safe governments and companies. Today’s yields are not that far off cash rates, but they have the benefit of locking in a long-term gain over cash.

Our market-leading alternatives portfolio (employing strategies that look to diversify from traditional assets) is designed to deliver a ‘cash+’ return. And while the rest of the portfolio will be in equities and lending to smaller companies, which can be a little uncertain over the short-term, the quid pro quo is that they give you the best chance of reaching your savings goals once the period of an uncertainty passes. It’s put together to beat cash, as long as you are patient.

Resisting the temptations to move long-term investments pots into cash puts you on the right side of how the world works.

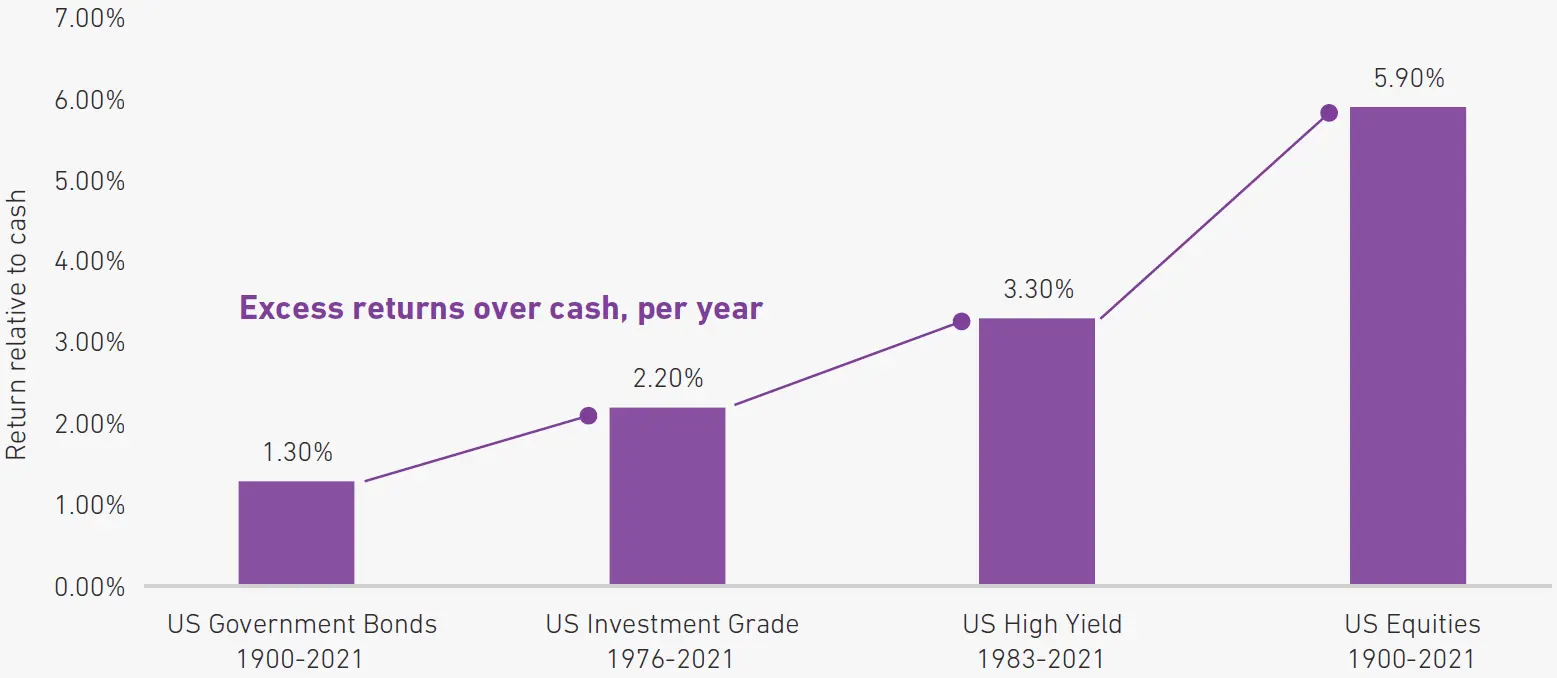

Cash is the lowest common denominator

The financial assets you are investing in are just a contract between you and a company or government. What’s key is that to tempt you away from cash, they need to offer a better return. Additionally, the risker the company or government is, the more return you should receive. This is the natural order in investing, and one you can use to your benefit by staying invested over the long run.

According to a long-term study2, since the 1900s investing in US companies has delivered a return of almost 6% per year higher than cash. But it’s not just the ‘riskiest’ investments either. Lending to Uncle Sam has delivered returns over 1% higher than cash. It might not sound like a lot, but if cash can’t even win against the safest investments out there, why would you hold it?

Average returns of individual asset classes vs cash over the long run

Discover more

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.