Quarterly Rebalance Commentary

Overview

Our last portfolio rebalance in November 2023 was followed by upbeat and positive sentiment across the market.

Economic data released in November brought optimism back to markets. As inflation showed signs of softening, central banks signalled the end of the hiking cycle, allowing investors to breathe a sigh of relief. This translated into a generous equity market with a month-end gain of 9% in the S&P 500, which marks one of the best November gains in a century for the index. Thanks to the large technology stocks, the Nasdaq 100 also grew almost 11% in the month, up from three consecutive months of losses. Equally, the fixed income market reacted positively to the promise of rate cuts in 2024, and global bonds underwent their fastest surge since the 2008 financial crisis.

The healthy backdrop continued into December, as fixed income and equities maintained their upwards trends. In the bond market, falling yields started providing significant capital gains; for instance, the Gilt maturing in 2061 saw a 25% appreciation in the month. In the equity market, large cap in the US climbed 5%, but with slightly less help from the Magnificent Seven; small cap also shone, proof of which was the Russell 2000 index’s 14% rise. This “Santa Rally” moved all major asset classes into positive territory for the year, a stark reversal of the disappointing returns available for investors in 2022.

In January, economic data continued to convince investors that central banks have reached the end of the rate hike cycle. Data out of the US showed stronger-than-expected GDP growth, and equity markets soared once more, seeing the S&P 500 reach a new all-time high. Meanwhile in Europe the Red Sea disruptions added to an already struggling manufacturing sector and economic growth in China continued to slow, with deflation adding more pressure to the country’s property crisis.

Core investment views

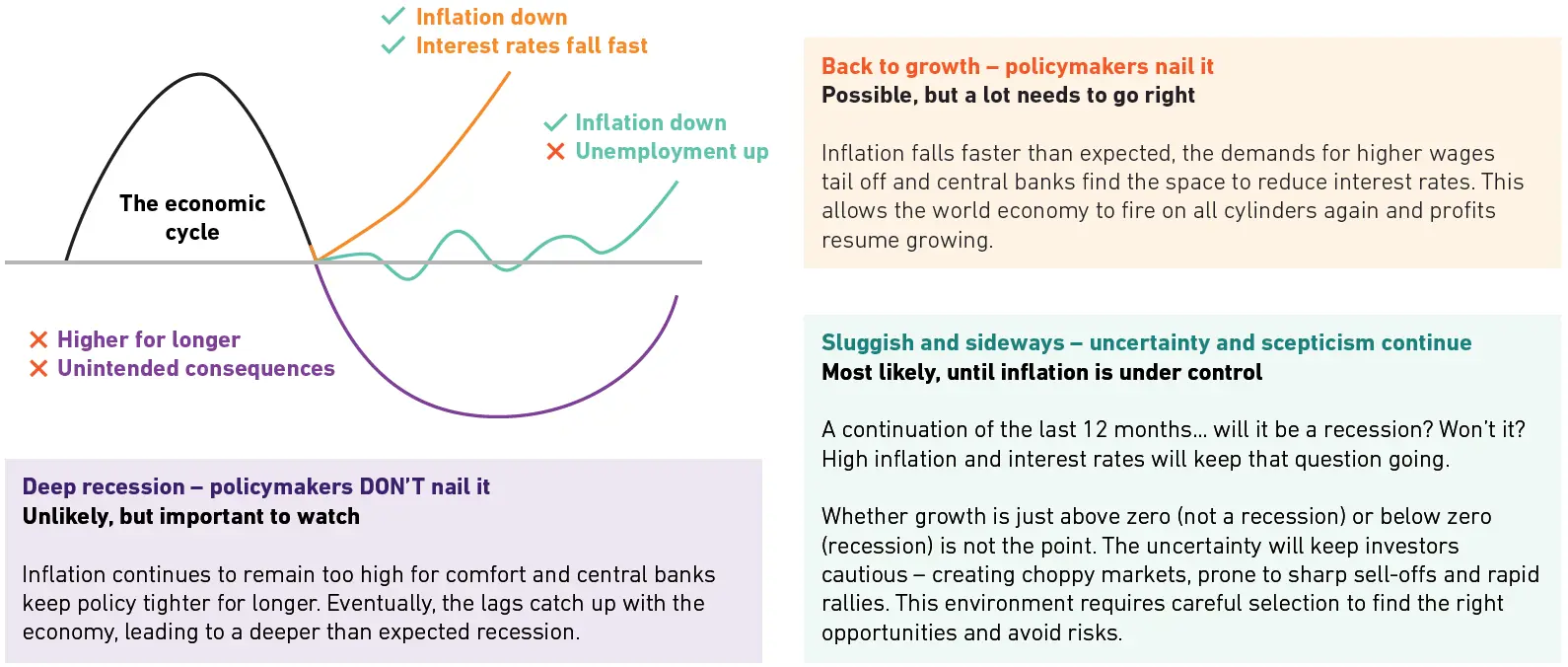

Despite the general optimism, it would be foolish to adopt a fully positive stance at any point in time. Even in a largely positive market, it is important to make sure no stone is left unturned to avoid any surprises on the downside. That is what we’re doing at 7IM - our properly diversified portfolios enable us to grow in every kind of environment:

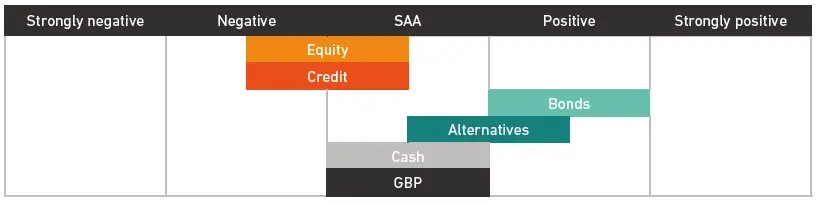

Tactical Asset Allocation

Headline Asset Allocation

In an environment with lots of uncertainty and a lack of confidence, we want to make sure portfolios are insulated against shocks, while still generating sufficient returns to make investing worthwhile. And we think our portfolios are set up to do just that.

Portfolio positions

There’s no one answer… When managing a diversified long-term portfolio, there shouldn’t be a single ‘big’ call. For an outlook which calls for selectivity, especially in the medium and short term, we’re finding lots of different opportunities – both to protect capital and to grow it.

| Long term: Thematic | |

|---|---|

| Healthcare companies | Stable earnings when others are seeing uncertainty |

| Climate transition leaders | Uncorrelated to short-term economic cycle |

| Alternatives | Defensive and diversifying |

| Metal & mining companies | Cheap and stable businesses. Short-term volatility, but profitable long-term |

| Medium term: Opportunities | |

|---|---|

| Finding pockets of value in the US | Investing in the most dynamic parts of the US economy |

| Tilt to UK Large Cap | Reduce domestic UK exposure while the economic uncertainty remains |

| AT1s | Attractive returns from here |

| Short term: Portfolio risk appetite | |

|---|---|

| Underweight equity risk | Reduce equity exposure as returns will be limited for the time being |

| Overweight bond duration | Bonds can do well if inflation continues to fall |

Asset allocation changes

We have made the following tactical changes to portfolios in this quarterly rebalance:

• Small reduction in our Government Bond allocation, but remain overweight compared with our SAA.

• Reduction in our Healthcare Innovations position. This is a position we still like for the growth potential it adds to portfolios, but after positive returns this quarter, we are rotating into other parts of the market.

• Added some FTSE 250 exposure back into portfolios. Having favoured focussing on the larger cap FTSE 100 part of the UK market, this quarter we moved some of this allocation back into the mid-cap space.

Manager changes

This quarter, there was one new addition to portfolios:

• HSBC Global Emerging Market Government Bond Fund was introduced to passive and blended accounts. This passive instrument has recently been reduced in price to provide much cheaper access to this asset class, while tracking the index very efficiently.

• Premier Miton US Opportunities was added to Active mandates in exchange for the previously held passive US equal weight position. The fund managers have a proven record at selecting profitable companies from all parts of the US economy, with very little overlap against passive large cap US exposure.

• JPM Emerging Market Income Fund was selected as a new addition for Active and Income focussed portfolios. This strategy targets high quality companies in Emerging economies that have a history of paying shareholders a dividend – something that demonstrates strong corporate health and governance in the region.

• iShares Japan Equity ESG Index Fund has been added to passive and blended mandates as part of the continued effort to decarbonise strategic allocations while managing risks associated with poor governance and sustainability.

• L&G UK Mid Cap Index Fund was brought into Blended portfolios. This provides exposure to the FTSE 250 section of the UK equity market.

Please note: All of the comments in this document refer to the models we run on the 7IM platform, but the models are also available on a range of other platforms. As much as possible, we try to replicate the models we run of the 7IM platform across all platforms, but due to differing security availability, not all of the points outlined in this document may be relevant across these platforms. If you are unsure whether certain changes apply to models on a specific platform, please reach out to a member of the team.

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.