Questions about COVID-19

The world is facing up to a winter with COVID-19.

While that’s not great, it’s important to note how much better prepared we are now for the virus. PPE is no longer in short supply. Medical treatment has improved. Test-and-trace is more effective. We know what we’re dealing with.

As this pandemic plays out, we will monitor the economic situation and act decisively if things change.

In March, we feared COVID-19 could be a re-run of the deadly Spanish Flu from 1918, and the level of restrictions reflected that. The last seven months have shown us that this is not the case. We also know that the virus can be defeated – just look at East Asia. So while the recent increase in case numbers is meaningful, we won’t see a re-run of March-April this year.

One of the strengths of our investment process is the framework through which we make our decisions. It ensures that we remain well informed and ready to take measured action where needed, for the right reasons. As this pandemic plays out, we will monitor the economic situation and act decisively if things change.

We’re still optimistic about the prospects for global economic recovery, but we know that recent headlines challenge our view. We’ve tried to answer the most common questions below.

Are we worried about a market panic over rising COVID-19 cases?

No. We think that the fundamentals for a strong global economic recovery are still in place, as highlighted by a series of strong earnings reports from major companies this week and an incredible 33% (annualised) jump in US GDP. Over the long term, that’s what will matter for portfolios. We have never thought that the path ahead was going to be smooth for growth assets – especially with a US election looming.

Our base case scenario assumed that any resurgence in cases would look like hotspots scattered across a map, which would remain local and manageable, allowing the broad global economic recovery to continue. And indeed, the current restrictions are still relatively limited to Europe. Asia and the US are not in the same situation.

As we’ve said before, we think that the impact of a huge wave of fiscal and monetary support across the world is more important for investors than the short-term impact of COVID-19 restrictions. While restaurants and bars closing make the headlines, it’s the continued functioning of other sectors – construction, manufacturing, financial services, healthcare – that actually drive the economy. They are in good shape as consumer demand starts to pick up.

Together with our optimistic view on treatments and vaccines, we still believe that the probability of an L or U-shaped economic recovery is low. The V/V+ shaped recovery remains our base case.

Do we still believe in ‘Surge and Burnout’ given the recent spike in COVID-19 cases?

Yes. In Europe, new hospital admission and death numbers are only about one fifth and one tenth of the peak numbers in March/April, respectively. This reflects much higher testing rates, the lower average age of patients and better treatments for those who are hospitalised. Although hospital admissions and deaths will likely continue rising in the coming weeks, they’re most unlikely to approach levels seen early in the pandemic.

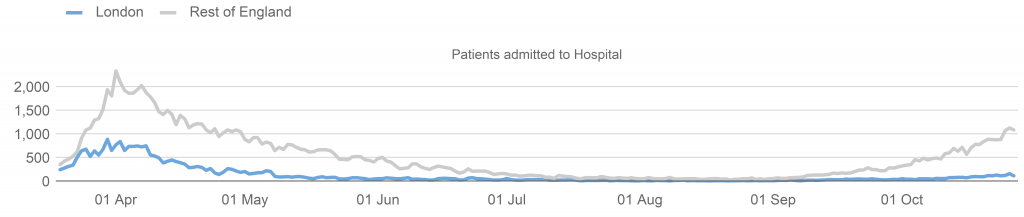

We also see signs that areas with high initial infection rates at the start of the year (the Surge) are not seeing cases rise in the same way as other regions, suggesting that some degree of Burnout has taken place. London is a good example of this, as shown in the chart. In April, London had around one third of total UK hospitalisations, while through September and October its share has been less than 10%.

People in Hospital with COVID-19

Source: https://www.london.gov.uk/coronavirus/coronavirus-covid-19-numbers-london

Do you still believe that the virus is less of a threat than the headlines are suggesting?

One of the key takeaways from our Surge & Burnout White Paper was that COVID-19 is not an equal opportunities disease. We still believe this is the case. The severity of the disease varies significantly between individuals (for some it is life-threatening and for others it is symptomless), while some individuals are far better at spreading the disease than others – think children in a playground or students in halls of residence. The idea that there are differences in people’s susceptibility and their ability to transmit the disease is not controversial.

This is important because the initial models for herd immunity assumed that everyone was equally susceptible to the virus and that everyone mixed randomly with everyone else. This is not how the virus spreads through communities in the real world. The virus targets the most outgoing (young) and the most susceptible (old) people first. Once infected, these individuals act as a barrier to the next potential cohort of people. This means the virus will find it much more difficult to spread going forward.

This characteristic brings down the threshold required for herd immunity from near 70% to between 20-40%. And in areas like New York or Johannesburg that suffered large enough initial surges, the research suggests that the disease will struggle to take hold a second time.

What about the new lockdowns in Europe?

The rise in cases in Europe is significant: the registered number of daily new cases across the continent is now almost three times larger than in spring. Again, though, most new cases are in those regions that were spared during the first phase of COVID-19 – this is a belated ‘first wave’ for many areas.

In response, most European governments are tightening restrictions on restaurant/bar visits, cross-country travel and social gatherings. Compared to earlier this year, the new raft of measures is less stringent and is not open-ended – most have been put in place for around one month.

The lesson from earlier this year was that the quickest way to stem the virus was through national lockdowns, but these have catastrophic economic and market consequences. While the new lockdown measures sound scary, the world is very different now.

We also know that economies are strong enough to snap back as soon as those measures are eased – over half the people who lost their jobs around Easter have already returned to work. We’ve learnt that governments around the world will ensure their economies can weather the storm.

And finally, we know enough about the virus such that the lockdown measures don’t need to be indefinite – we have ‘circuit breakers’ instead. And note that the two most economically important regions, the US and East Asia, are not going through another shutdown. Instead, the stage is set for a rapid and broad economic recovery as we move through 2021.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.