Are tech stocks hot again?

It’s been a great time for the big US tech stocks recently.1 Microsoft is up 10% to 3 February, Apple 16%, Alphabet 23%, and Amazon 34%. Meta is up 57%, including one day in February that saw a 23% rally!

Yet it’s also been rough for the big US tech stocks recently. Since the end of 2021, Microsoft is down 21%, Apple is down 15%, Alphabet is down 25% and Amazon is down 32%.2 Meta is down 44%, including a day in February 2022 that saw a 27% fall! It just depends on what you define as ‘recent’.

So what’s next? Will this year’s rally keep going? Or will the downwards slide of 2022 resume?

Cards on the table: we’re in the latter camp.

Still a concentration calamity waiting to happen

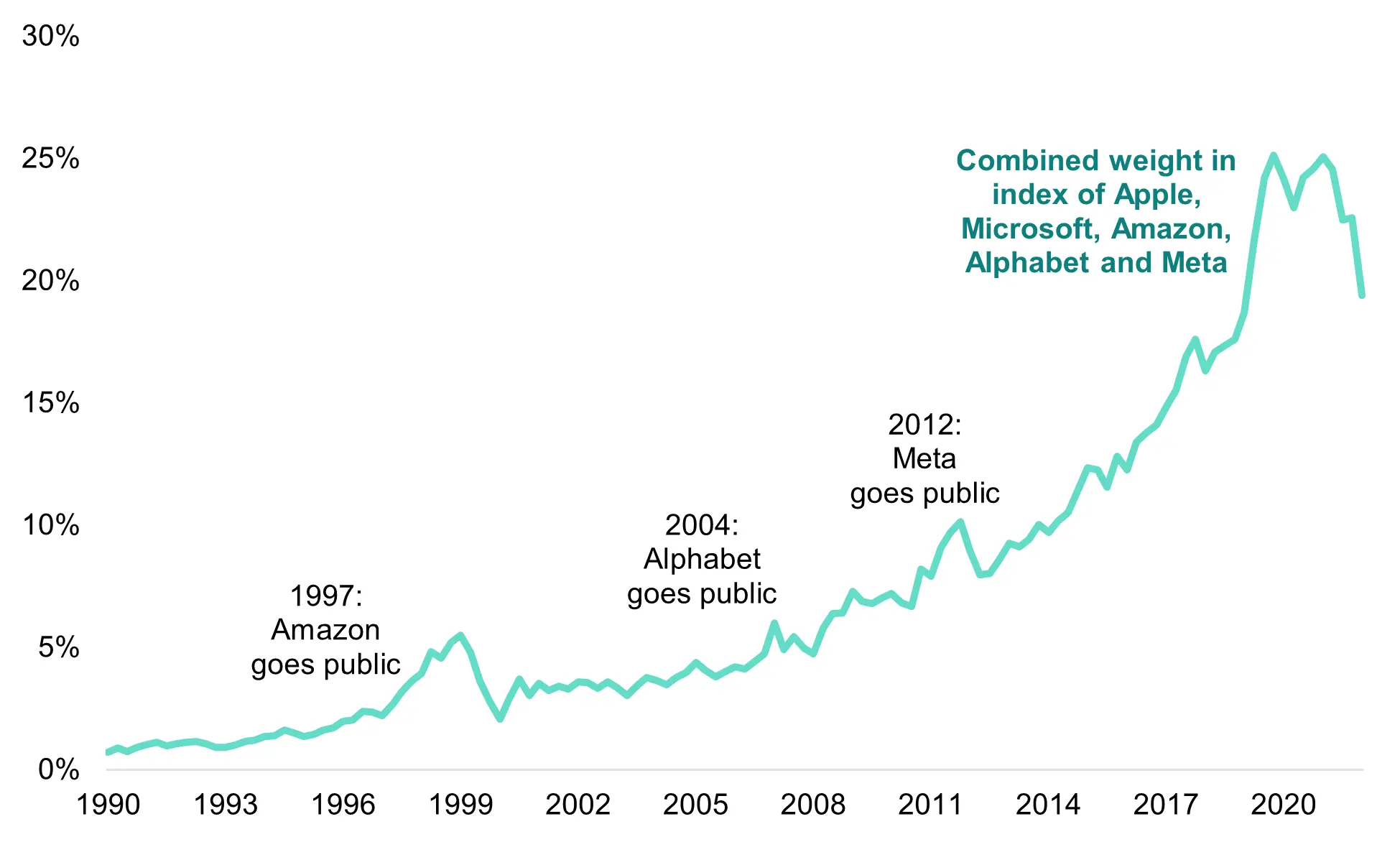

Simply put, the US equity benchmark – the S&P 500 – is still dominated to an alarming degree by a few companies. The chart below shows the rise of the big five tech companies since 1990 (when actually, there were only two: Apple and Microsoft).

Source: Bloomberg Finance L.P./7IM

When we were growing concerned in 2021, these stocks represented more than 25% of the entire index. And even after a brutal 2022, these five are still 20% of the S&P 500.

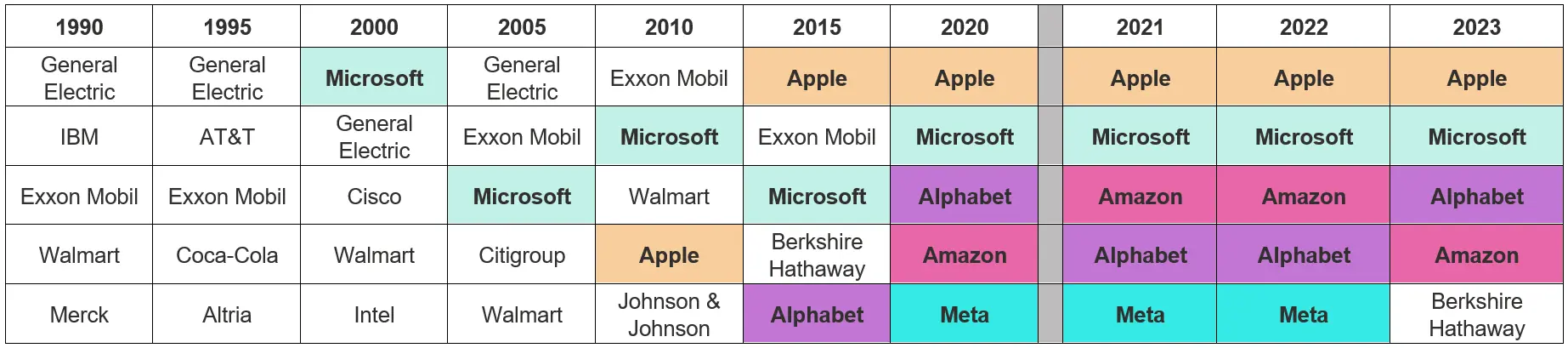

Of course, a high concentration in a few companies doesn’t necessarily mean that those companies will do badly. Look at the table below.3

Five largest companies in S&P 500 at the beginning of year

Source: Bloomberg Finance L.P./7IM

In 1995, the largest five businesses were an industrial conglomerate (General Electric), a telecoms business (AT&T), an oil major (Exxon), a drinks provider (Coke) and a tobacco company (Altria). Pretty diverse business models!

Even as recently as 2010, Microsoft and Apple were accompanied by that same oil major (Exxon), a retailer (Walmart) and a pharmaceutical company (J&J). Still some differentiation. But ever since 2015, the top five have been becoming techier and techier – with lots of similar drivers.

If something does hurt technology stocks, the pain is extremely focussed at an index level – in a way that it hasn’t been previously.

Not enough to go round

Aside from the investment problem of concentration, there’s also the matter of the business problem of concentration. One great way to be successful in business is to be exceptional in an area where competition is limited. You can scale quickly and dominate a market.

All of the big five tech companies did exactly that, in different areas. It made them the massive success stories they are today. Apple in cool smart devices. Microsoft in boring but necessary enterprise software. Alphabet in search. Facebook in social networking. Amazon in online retail.

But they’ve now got a problem. Each other.

As they’ve grown, each of the big five has begun to expand its business interests. And once they move outside their core initial product, they’re beginning to butt heads.

Amazon found it easy to disrupt real world bookstores. But it’s less easy to dominate cloud computing when you’re up against Microsoft and Alphabet. Driverless cars might be exciting, but the best talent is being split between Amazon, Alphabet and Apple (and indeed Uber). Or look at the recent excitement around Microsoft-owned ChatGPT, prompting Google to launch its own Bard tool.

Arms races can be fantastic at incentivising innovation: the US-Russia competition to get to space resulted in exponential acceleration in rocket technology, for example. Competition can be great for the end consumer. But it won’t be so good for profit margins at the tech companies – the USSR ultimately went bankrupt.

Untested in an economic recession

Finally, there’s the recession question to contend with. There hasn’t been a genuine recession in the USA since the ’08 financial crisis (we discount COVID-19 as too short, and too weird – consumers ended up with more money at the end of it!).

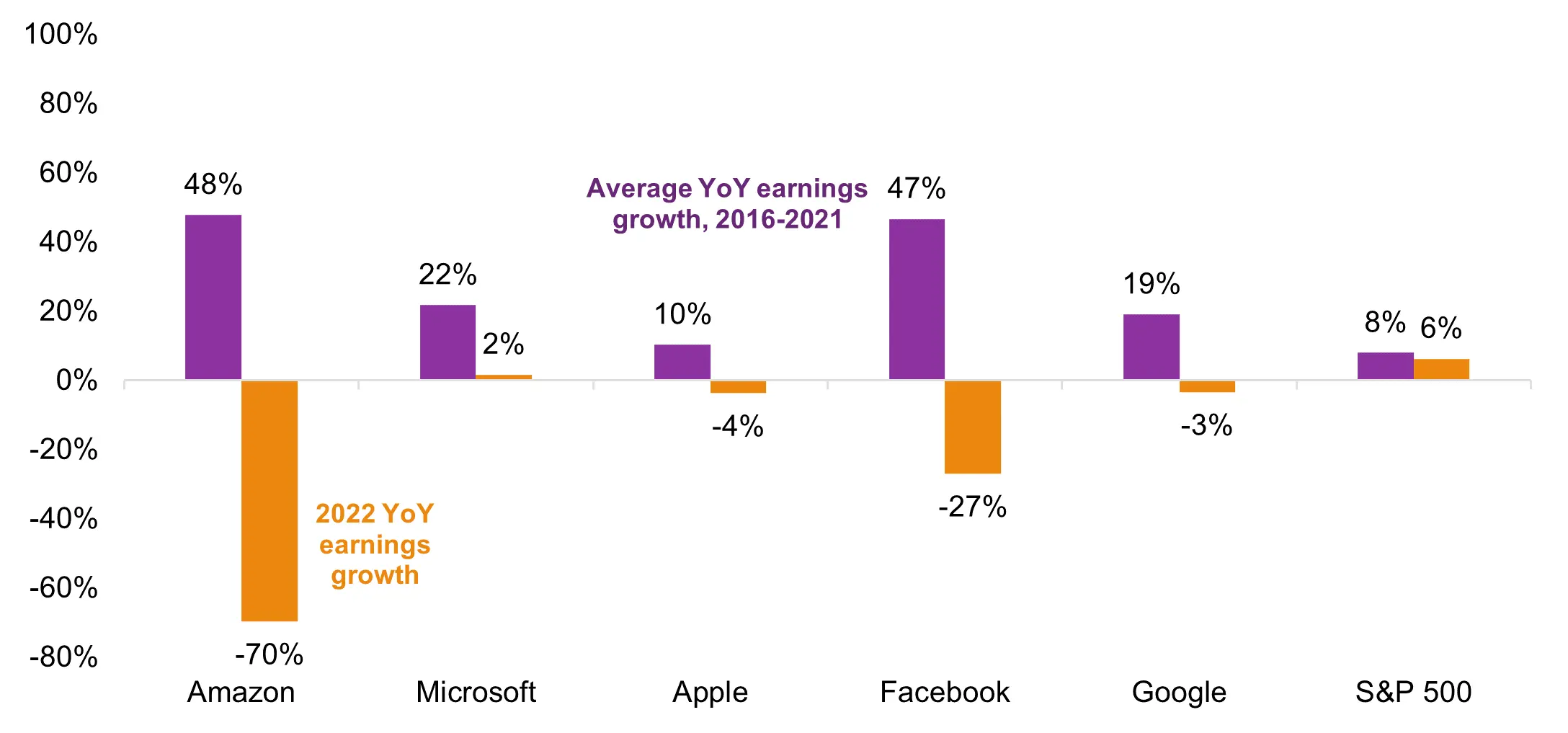

At the start of the year, tech analysts were expecting earnings in 2023 to be better than in 2022. But if a recession does come, that is most unlikely. Not delivering on the double-digit earnings growth investors have become used to is likely to be a problem for the big five. Between 2016 and 2021 (purple in the chart below), every one of the big five grew earnings more quickly than the S&P average. In 2022, none of them did. And their prices suffered accordingly.

Source: Bloomberg Finance L.P./7IM

So is worse to come? Well, the big five don’t know how susceptible they are to a sustained fall in demand. Advertising revenues will fall – but how much? Device demand will fall – but how much? Businesses with existing contracts will go bust – but how many?

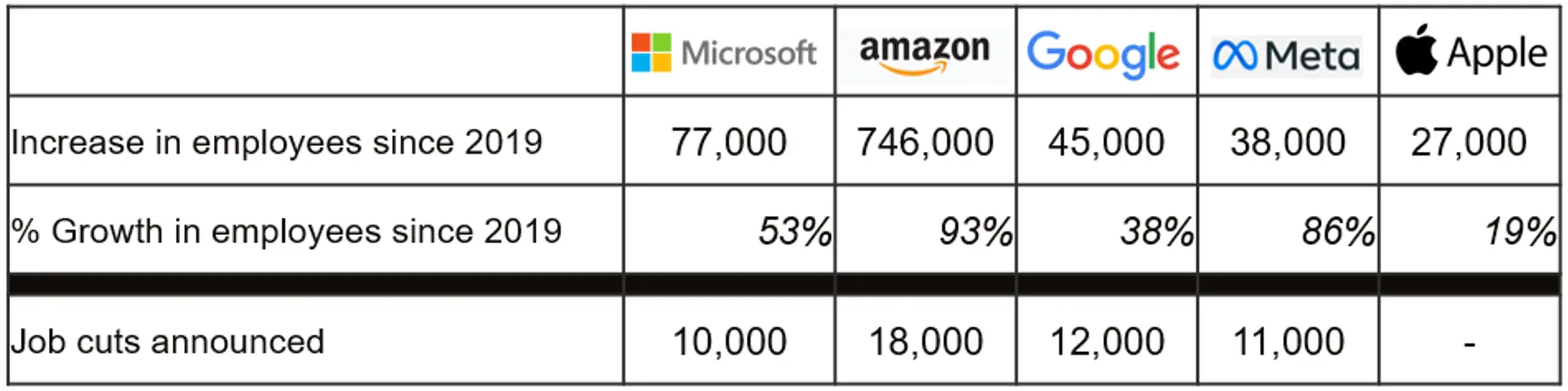

These are difficult questions, and the companies themselves don’t know what to do. We’ve seen some job cuts announced already, but as the table below shows, for most of the big five, they’re only a small portion of the people they’ve hired since 2019. Far more could be needed.

Source: 7IM & Company Annual Reports / Data from past 6 months

The pain isn’t over

We’ve been concerned about the giant US technology companies since the autumn of 2021. We allocated money to a variety of other areas, such as healthcare companies, the FTSE 100, and Berkshire Hathaway. In April 2022, we reiterated that view (https://www.7im.co.uk/private-client/news-views/thinking-differently-about-us-equity-markets-in-2022).

In fact, for the last 18 months or so, we’ve held less than 10% of our total equity allocations in the US equity index. Given that most passive global equity products have around 70% in US equities, that represents a meaningful difference in opinion.

And our opinion hasn’t changed. Nor will our portfolios.

1 Data from 31/12/22 to 03/02/23

2 Data from 31/12/21 to 03/02/23

3 Here’s a cool animated version https://www.youtube.com/watch?v=bOPeRnaVezQ

You can download the commentary as a PDF here.

We’re excited to announce that 7IM for Private Clients, London, has now merged with, and rebranded to, Amicus Wealth Management.

This marks a vital step forward in our mission to deliver the very best wealth management for our clients.

While our name has changed, our values and commitment remain the same. We’ll continue to provide personal, bespoke financial planning, built around you.

Explore Amicus Wealth Management