Monthly commentary

Monthly Musings: Discipline is easy in theory…

There are two tricks to investing. Knowing why you’re buying something in the first place … and then sticking with the investment long enough for the results to materialise.

It’s actually the second part of this that’s toughest. Coming up with a sensible investment idea is … well, it’s not easy, but it’s doable. But there’s no investment case in the world that is SO right, SO clever, SO robust that the market won’t, at some point, make you look stupid.

There’s a great academic bit of work on this produced in 2021* called “Even God would get fired as an active investor” (link below), looking at how painful it can be to be a long-term investor. Long story short, you’d have lots of double-digit paper losses even if you KNEW you were picking the BEST performers for the next five years. And that’s without even considering the various headlines and shocks that also cause panicked selling.

A great recent example is US tech vs. European banks** over the past few years. A classic battle of old-world vs. new world. Some of the oldest, most traditional companies – Deutsche Bank, UniCredit and Societe Generale were all founded at around the time the American Civil War ended – up against some of the newest, most forward-thinking businesses – the NASDAQ 100 index only started in 1985, and many of its constituents for far less time.

Think about the situation at the start of 2021. In 2020, the 29 banks in the index combined made €60 billion in profit. Apple made more than that on its own. Banks were at the heart of worries about COVID and debt, being told to cancel their dividends in order to ensure survival, while tech stocks were benefitting from all of the work-from-home readjustments.

Imagine, though, you’d had the foresight to say “well, this is as bad as it gets for banks and probably as good as it gets for tech stocks. I’ll buy banks”. You’d have been right! Since the start of 2021, European banks have risen by 272%. The tech-heavy NASDAQ index is up 72%.

But, I wonder, would you have been able to deal with the ride? You’d have been able to hack double digit underperformance in two of the last four years? You’d have held your nerve through more global lockdowns in 2021? Through the invasion of Ukraine in 2022 (right on the doorstep!)? Through the actual, literal default of a European bank (Credit Suisse) in 2023? You’d have ignored the AI hype in 2024 and so far in 2025?

It’s like strict dieting. On warm Tuesday evenings, a salad is actually pretty appealing. But on a Saturday night, when the takeaway is calling, the theory goes out of the window. As ever, this comes down to managing emotions – which you can’t do through explanation and analysis. With dieting, the trick might be to avoid going anywhere near the high street at the weekend (or avoiding keeping snacks in the house).

With investing, I’m afraid it’s a bit more complicated … a never-ending battle between important fundamental information and emotion-triggering noise.

* https://alphaarchitect.com/wp-content/uploads/2021/08/Even_God_Would_Get_Fired_as_an_Active_Investor.pdf

**we’ve specifically invested in European banks in the past – and we’ve got tactical exposure to the broader global financials at the moment.

Chart of the month

Investors are quick to apply labels to a business, a sector, or even a whole country!

This can be for the good (“AI is the future”) or the bad (“the UK is uninvestable!”) – and while they’re hardly definitive analysis, they can hang around for a long time.

For years, one of the most popular themes has been the “death of the high street store”. Investors and shoppers have written off physical retail stores; consider the failure of companies of Woolworths, Toys R Us, the rebrand of WH Smiths (RIP).

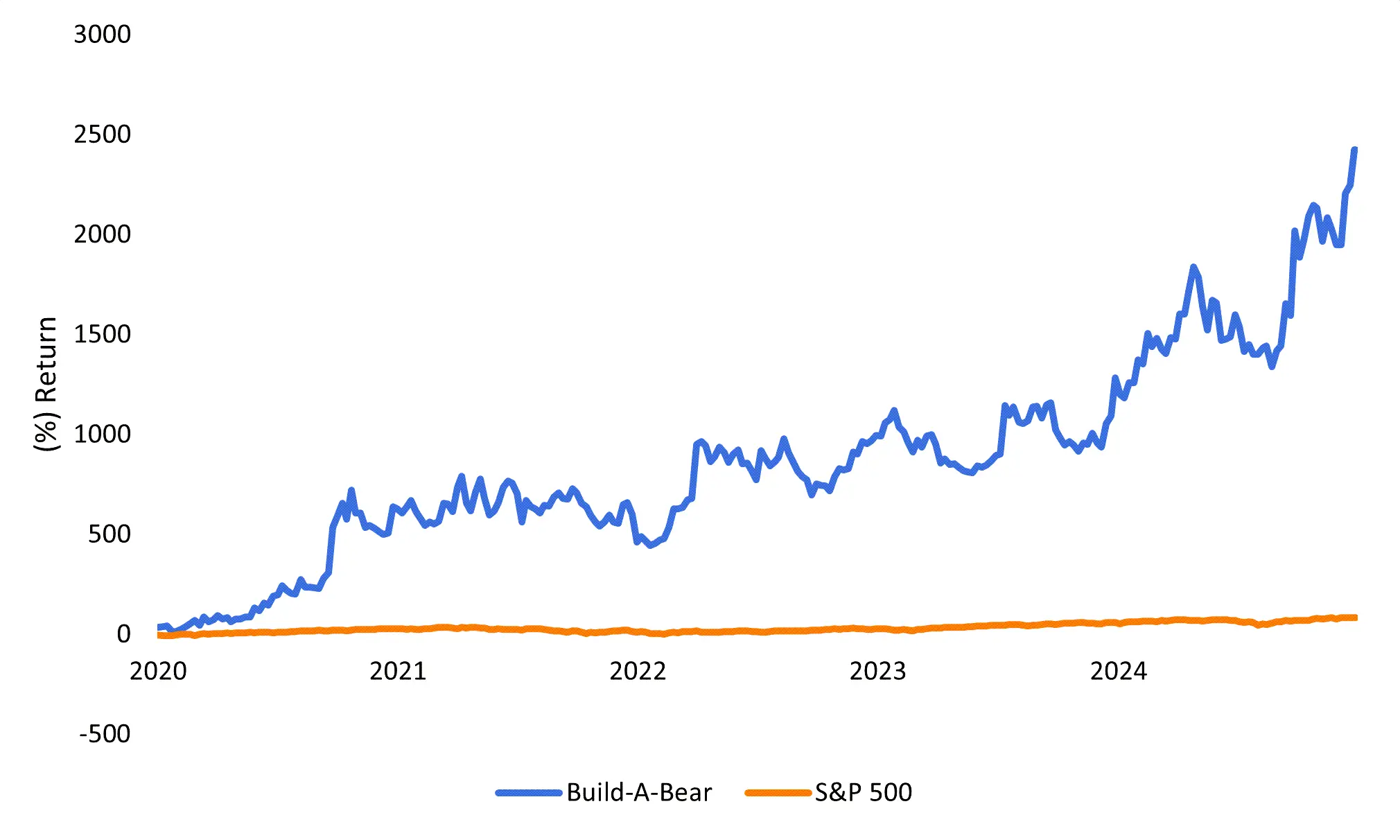

But there’s a cute and fluffy counterexample of where labels can often go wrong; Build-a-Bear Workshop. They’ve doubled down on the experience factor. Children come in, have a full consultation on scents, sounds, outfits of their teddy bear, then have it made. Kids love it – something that’s all about them. Adults love it – something physical in a digital world.

And its share price has soared – in the last five years, the S&P 500 has doubled. Build-a-Bear has risen by 20x! Not bad for a “dead” business model …

Source: Factset

August Markets Wrap

A summer slowdown failed to materialise in August, as equity markets generally ended the month higher. Portfolios diversification beyond the US was rewarded once again, with China, Japan, Asia Pacific and Europe leading returns, as they have since the start of the year. The latter’s performance was all the more impressive, given that the German and French markets struggled due to poor economic news coming out of Germany and with the French Prime Minister calling for a vote of confidence. AI dominated the headlines once again and technology related stock performance reflected this, with the tech heavy NASDAQ index setting new highs, assisted by positive news on corporate earnings.

In fixed income world, politics remained on the forefront. From Trump trying to sack Fed members, to increasing confidence issues in the UK and France, politics is having an impact on long term government borrowing rates which continued to creep up in August.

Notwithstanding this, our approach of applying wide diversification in bonds, as well as equities, is paying off, with even most lower risk portfolios, which tend to have a higher allocation to the asset class, delivering positive returns over the month.

Market Moves

Equities |

10 Year |

5 Year |

1 Year |

|

FTSE 100 |

7% | 11% | 11% |

|

S&P 500 |

14% | 17% | 15% |

|

MSCI Europe ex-UK |

7% | 12% | 9% |

|

Topix |

8% | 16% | 4% |

|

MSCI Emerging Markets |

5% | 7% | 16% |

Government Bonds |

|||

|

Gilts |

0% | -6% | 1% |

|

US Treasuries |

1% | -2% | 5% |

|

Bunds |

0% | -2% | 4% |

Currency |

|||

|

USD v GBP |

1% | -2% | -8% |

|

EUR v GBP |

2% | -1% | 1% |

|

JPY v GBP |

0% | -8% | 3% |

Source: Bloomberg. Data as of 29/08/2025

What we’re watching in September:

- 8th – French Government confidence vote

- 17th – Federal Reserve Meeting – Will Trump get his way?

- 18th – Bank of England Rate Decision

More from 7IM

We’re excited to announce that 7IM for Private Clients, London, has now merged with, and rebranded to, Amicus Wealth Management.

This marks a vital step forward in our mission to deliver the very best wealth management for our clients.

While our name has changed, our values and commitment remain the same. We’ll continue to provide personal, bespoke financial planning, built around you.

Explore Amicus Wealth Management