Monthly commentary

Monthly Musings: From school playground to the stock market

We start seeing society take shape from early on. At school, children start to show different inherent traits. There will be the attention-seekers, the shy, the athletic, the book smart, the street smart, the lazy, the savvy and the class clowns…

Fast-forward a couple of decades to your school reunion, and you’ll still recognise many of those traits you saw when you were kids.

But the interesting part is that it’s quite difficult to predict success based on those personality traits, because it’s up to each individual to use such traits to their advantage.

The same happens with equities across the globe. Of course, success doesn’t have one definition, but for investing it means performing above peers over the long term – those that have weathered the choppy environments of the past years or even decades are the winners.

So, looking at the UK’s benchmark index, the FTSE 100, if we asked you to think of five stocks, which ones would you pick? Our guess is your list would contain some of the following names: AstraZeneca, GSK, BP, Shell, HSBC, Unilever, Rio Tinto.

That would make sense, given that these companies are among the ten largest FTSE 100 companies based on market value.

But look deeper into this index and you’ll find the hard work of less visible names shining through.

Let’s put it this way: they’re not in the oil business, drug manufacturers, mining companies… They’re visible in a different, more indirect way. And if you don’t use them on a daily basis, when you do, they’re really useful.

Take JD Sports Fashion, for example. In the past two decades, the sports fashion group has delivered its shareholders an annual return of 24% to its shareholders. Rightmove, the online property portal, has returned 18% to investors in the same timeframe.

Outside of the high streets, the companies delivering best value to their shareholders sit in the industrials space, many of which rewarded their shareholders more than 14% annually over the past 20 years, which is the value Rio Tinto has distributed.

Meanwhile, GSK boasts a 6% annualised return, Shell 8%, BP 5%, Unilever 11%...*

In the end, as a society we need the miners, the banks, the pharmaceuticals… but society wouldn’t work if we also didn’t have the successful fashion companies and online house portals.

When you’re looking for growth, diversity is a key ingredient… regardless of whether that’s across society or the stock markets. And the FTSE 100 is no exception.

* Please note this is not investment advice. The references made to companies are only intended to be an illustration of the power of diversification. Data source is Bloomberg.

June Markets Wrap

In investing, concentration is a danger and the Nvidia stock tells a story that may turn out to prove just that. The most valuable stock on Earth, as it has been called, overtook Microsoft and Apple, reaching a market value of $3.34tr in June. However, this success was short-lived as the stock lost about $550bn in three trading sessions, amid concerns around artificial intelligence reaching a peak. Of course, that still leaves it with around $3tr to play with… but it shows how quickly things can change.

Because of their size, any fluctuations in the giant technology companies’ stocks result in a significant shift for the market-cap weighted benchmark index. These events are a good reminder of how portfolio diversification should always remain central to any investment strategy.

In the UK, the attention has been centred elsewhere. With UK voters hitting the polls on 4 July, it was highly unlikely that the Bank of England would steal the spotlight from politics and cut rates in June. After all, the central bank has kept rates unchanged at 5.25% since August 2023, and there was no major unforeseen event that prompted it to rush towards a cut.

That’s exactly what happened. And in fact, if anything finally suggested that the worst might be over is the fact that inflation hit the 2% target for the first time in almost three years. Food prices was the largest downwards contributor, but services inflation photobombed what would otherwise have been a perfect picture.

The effect of the UK election on the financial markets has been minimal, as expected. After all, with the exception of the Truss mandate, politics hasn’t meaningfully moved markets in a long time, and none of the potential election outcomes are expected to generate any extraordinary movements.

So, in this backdrop, the FTSE 100 remained relatively stable in the month.

But there seems to be no parallel between the elections in the UK, and those across some parts of Europe. A landslide win for the French far right in the European elections, coupled with the surprise call for a snap election in France, led to the worst week in two years for the French benchmark index CAC 40. French government bond yields also went up on the back of the event, and the spread between French and German bonds (the difference between the yields of these two securities) widened.

These political events in France alone were not enough to stop wider European stock growth, however, the MSCI Europe ex UK index still showed an 11% growth in the year. But the French elections have highlighted a picture of political stability on the other side of the channel, which UK investors have certainly welcomed.

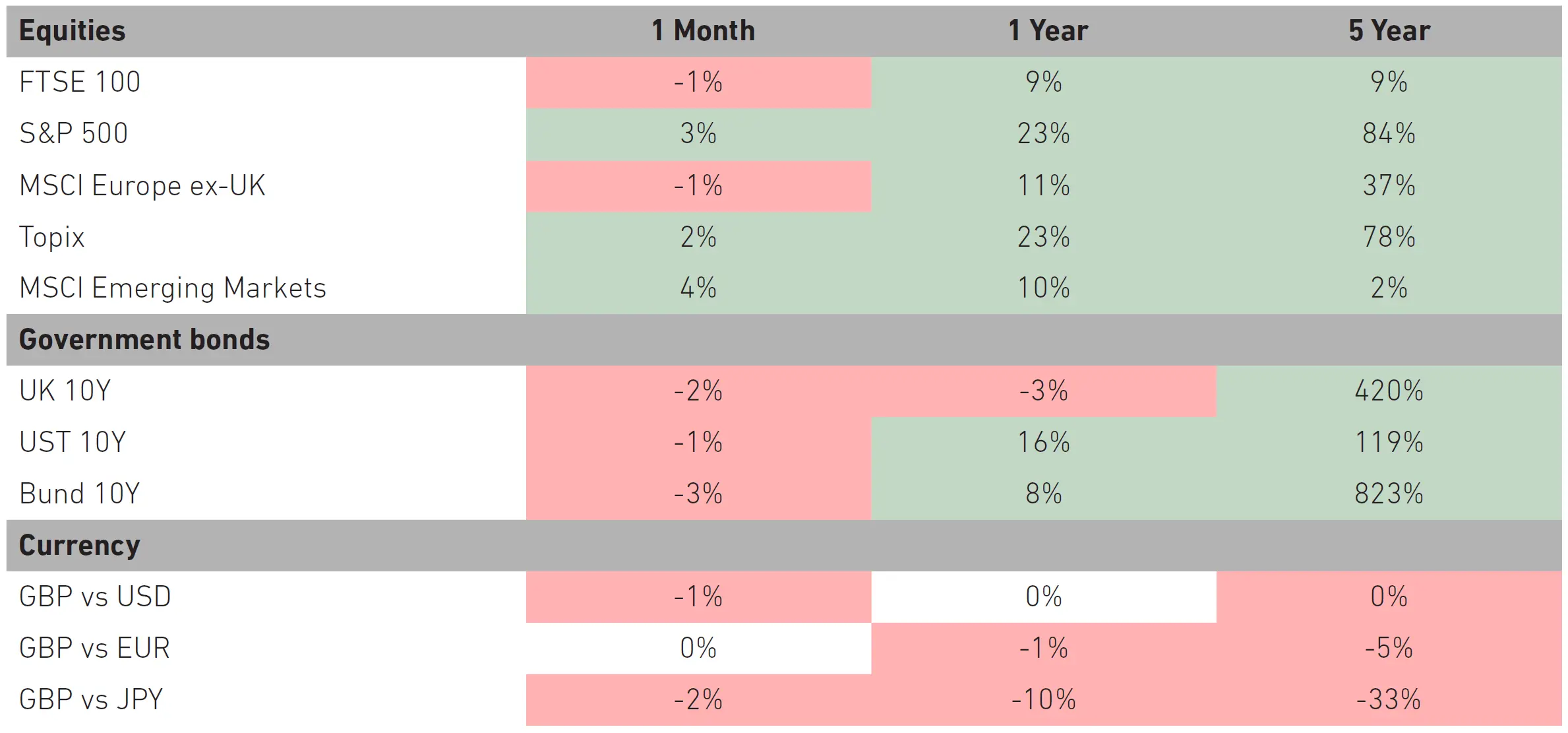

Market Moves

Source: Bloomberg. Data as of 1 July.

What we’re watching in July

- 4 July: UK Election. We’re watching it, and while it’s a significant event for UK citizens, it’s not likely to be one for markets

- 7 July: French election (second round): European asset prices have responded to the French political turmoil with volatility, so we’ll be following its effect on markets

- 14 July: Football comes home? Euro 2024 Final

- 17 July: UK inflation rate for June

- 31 July: Federal Reserve interest rate decision. Will we see the first cut?

You can download the commentary as a PDF here.

We’re excited to announce that 7IM for Private Clients, London, has now merged with, and rebranded to, Amicus Wealth Management.

This marks a vital step forward in our mission to deliver the very best wealth management for our clients.

While our name has changed, our values and commitment remain the same. We’ll continue to provide personal, bespoke financial planning, built around you.

Explore Amicus Wealth Management