Monthly commentary

“It’s quiet. Too quiet.”

A funny thing I’ve noticed is that, come the autumn, if stock markets are up, you know, a decent amount, people start to get a bit … twitchy. They start casting around for things to worry about – signs that something’s about to go wrong in the economy, or the bond market, or the Middle East (usually an easy target).

Perhaps it’s the feeling of being almost at the end of a long journey back from a trip away. Your coach to the airport showed up. Your plane took off on time. You got your bags quickly. And then boom. The taxi cancels, there’s a huge queue, and it’s raining. Horrible end to a holiday. Could it be that investors – fresh from their own summer jaunts – start seeing the investing year through the same lens? “Don’t mess up, don’t mess up, don’t mess up”

Or is it that we’ve all just watched too many horror films, and the idea of it being “too quiet” just doesn’t sit well … we’re looking for the monster behind the curtain. It’s the run-up to Hallowe’en after all.

This phenomenon is in full swing at the moment, with a bit of extra fizz due to the all-time highs* being recorded in markets all over the world.

And, because there’s so much data flying around, there are some great lumps in the drapes to point at. One of my favourites this year has been the 5% decline in cardboard box production in the US over the course of the year. The “spoooooky” spin on this is that companies are fearful of demand for their products, so dialling back their orders.

My slightly more … straightforward … view is that in a year where the US President called a huge timeout on trade for a couple of months, it’s no wonder there’s been a decline in the need for packaging. It was (to paraphrase Scooby Doo) the weird, unfriendly janitor the whole time.

For investors whose job is to find opportunities over the medium term, these late summer blues aren’t something to take too seriously (occasionally, as noted in the chart of the month, they give you a nice chance to pick up some bargains!).

On the Investment Team, we’re looking at the data we trust. We’re seeing interest rates falling and company earnings growing. We’re seeing inflation remaining contained, and economic growth staying positive. There are, of course, a few things which are worrying; some sectors look expensive, some governments have budgeting problems, and there are political troubles on every continent.

But, for us, the good outweighs the bad. It’s easy (even enjoyable) to get scared by a horror film. But you shouldn’t spend the next year jumping at shadows!

* We’re big believers that all-time highs aren’t anything to get excited about. A stock index is a collection of businesses that’s meant to grow over time. In fact, if it NEVER hits new highs, that’s when you should really worry!

Chart of the Month: Wake me up, when September ends?

There does seem to be something rattling around in the data about September market performance – going back to 1950 (in the US), September is the only month where the average return is negative! Of the 75 Septembers since 1950, 41 of them have been down months.

So, you can file this September’s 3.5% return as a rarity; it’s the best we’ve seen in 15 years!

Average S&P 500 Return by Calendar Month (%) Since 1950

Source: FactSet/7IM

September Markets Wrap

The US Federal Reserve cut interest rates for the first time in 2025, as inflationary concerns were superseded by perceived weakness in the US labour market. This may have helped to prompt the rally of over 3.5% in the US S&P 500, but this was superseded by Asian and emerging markets’ performance, with the S&P Pan-Asia index up over 4% and the Latin American equivalent up over 6%. This continues the trend year-to-date of strong EM performance, reflecting the more attractive valuations that exist in the various regions within this asset class.

Of course, politics continued to make headlines – and although the announcements on tariffs were largely shrugged off – the political backdrop in the UK, Germany and France is certainly weighing on sentiment. Bond markets are still reasonably calm, though, potentially as investors await the outcome of significant events such as the impending UK budget and uncertainty over the ability of the new Prime Minister in France being able to push through significant fiscal reforms.

Overall, equity markets globally exhibited positive returns (not always guaranteed in September!). With lower volatility in sovereign debt, the majority of bond markets were also able to rally, although those with higher duration (sensitivity to interest rates) struggled more than the shorter-dated versions, notably in the UK, as longer term government borrowing rates continued to climb. Notwithstanding this, all portfolios were also in positive territory, which continues the positive trend following the markets bottoming in April, post ‘Liberation Day’ in the US.

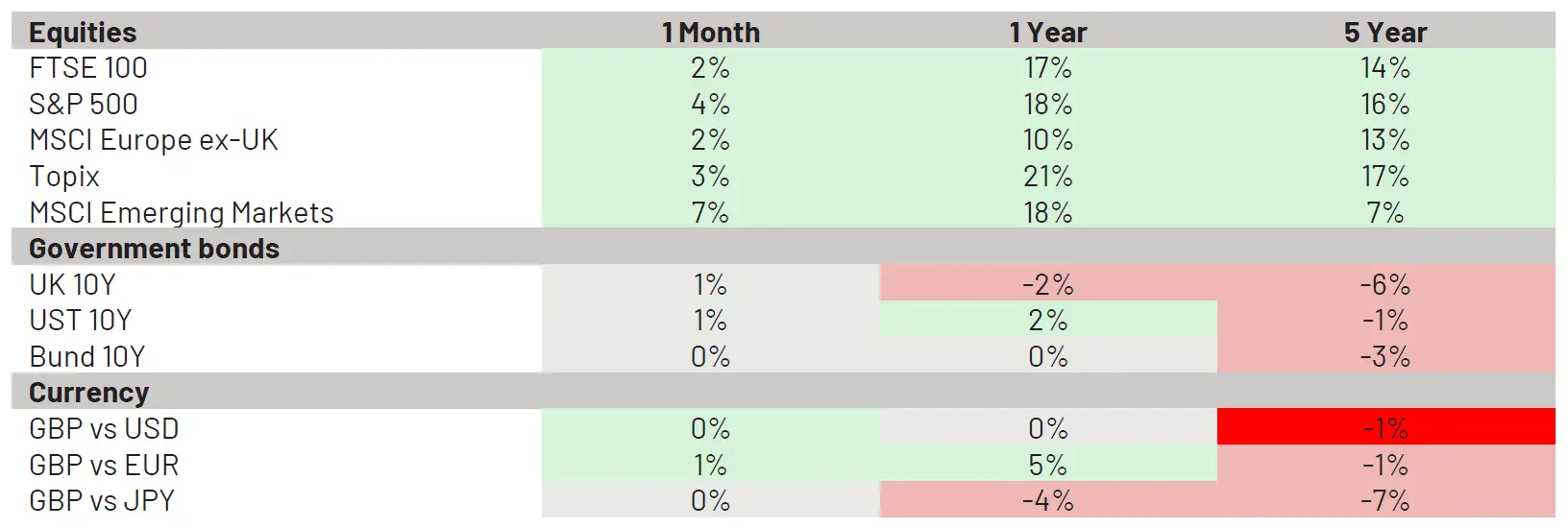

Market Movers

What we’re watching in October

- Ongoing – US government shutdown. The longer it lasts, the worse the collection of data gets.

- 14th/15th – all of the big US banks report their quarterly earnings

- 21st – Netflix reports Q3 earnings; if consumers really are struggling, they might cut subscriptions first

- 28th – Anglo American Q3 production report; how is the demand for industrial metals?

- 30th – ECB meeting.

More from 7IM

We’re excited to announce that 7IM for Private Clients, London, has now merged with, and rebranded to, Amicus Wealth Management.

This marks a vital step forward in our mission to deliver the very best wealth management for our clients.

While our name has changed, our values and commitment remain the same. We’ll continue to provide personal, bespoke financial planning, built around you.

Explore Amicus Wealth Management