Curious COVID behaviour

We’ve talked before about the lizard in our brains – the driver of our instinctive responses to stimulus – which the more rational, human part of the brain has to constantly overrule. And we’ve mentioned that the lizard is loss-averse; it hates the idea of losing money.

As investment professionals, it’s our job to calm down the lizard in clients’ brains. It’s important to realise though, that this is an ongoing task. It’s not enough to talk someone through a crisis – we have to be there for the after-effects too. It’s like the difference between being a surgeon, and being a personal fitness trainer. One fixes an acute problem, while the other is there to support a long-term lifestyle change.

It’s not about taking the lizard out of the equation – it’s about knowing how to offer support when the lizard is running riot.

COVID and cash

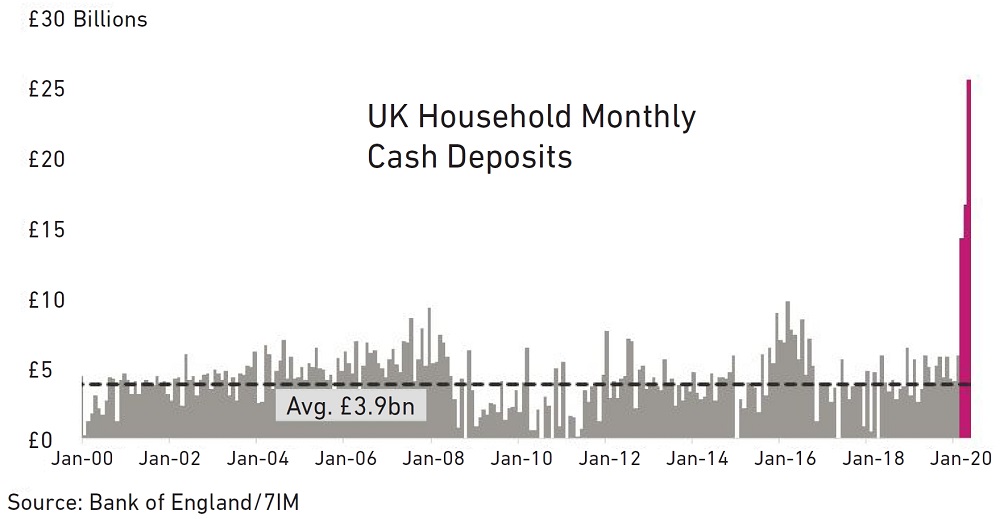

Over the last few months, UK households have been putting aside a lot more cash than normal. The chart below shows the total cash deposits into bank accounts by UK households every month – on average, the country saves around £4 billion a month. This sounds like a lot, but with around 28 million households in the UK it ends up being £140 put aside each month per family.

That changed once COVID-19 hit. In March, the UK put £14 billion of cash aside. In April, £16 billion more. In May, £25 billion. That May number means close to £900 put into bank accounts per household per month. It’s the same story elsewhere in the developed world.

This kind of behaviour, whilst understandable, is a risk to investment plans everywhere. It’s not as obvious as cashing out, but it is behaviour that still needs combatting with careful management and advice.

So why did COVID cause this? Partly, it’s because of the lack of things to spend money on. Lockdown forced people to curtail their normal spending on entertainment. We forget how much of a mark-up there is outside of your own front door – I know I got a shock when I received the first post-lockdown bill for a pub lunch the other day! Without impulse purchases, takeaway coffees and trips to the cinema, there was just a bit more cash to go around.

Now though, the shops are open. As are restaurants and pubs. But the savings trend is still likely to be well above normal in June, because COVID-19 has impacted the psychology of the nation as well as the economy. The crisis didn’t just affect our ability to spend, but also our willingness to do so.

Bad times ahead

Normally, we talk about controlling the lizard when faced with unexpected market shocks. The phenomenon here though is a little different – stockpiling is a bit more calculated, involving both bits of the brain, human and lizard.

This isn’t a market panic and the hoarding of cash isn’t a reaction to something that has happened already. Instead, people are trying to look to the future. We’re all hearing about the difficult road ahead, about job losses and tough times, and a lot of uncertainty. Social psychology reinforces it – when everyone we talk to is slightly worried, we become more worried.

This causes a slightly different train of thought. The lizard doesn’t panic about losing what it has now, it starts worrying about not having enough in the future. That scares the lizard, and the human comes up with a plan to save more.

So we start stockpiling. We saw this in the early days of COVID with supermarket shelves stripped of pasta and toilet roll. And now we’re seeing it in a broader economic sense. People are putting a little bit more money away, just in case. It’s happened before. Ahead of the Brexit referendum in 2016, cash levels started building too. Just in case.

Be careful about being cautious

There’s definitely nothing wrong with having a little money set aside – in fact it’s sensible to have a cushion for the unexpected. But when the unexpected starts happening, if you’ve planned properly, you shouldn’t need to increase the cushion further.

It’s not just staying invested which is important, it’s also key to keep adding to those investments. We worry when clients abandon their investment plans, but we worry just as much when we see clients suggest abandoning their savings plan in order to preserve cash.

Clients who’ve been persuaded not to sell their existing portfolio often jump to the next ‘lifeboat’ – stopping regular savings “just until the crisis is over”. Piles of cash are seductive; it’s easy to stop putting money into a stocks and shares ISA, but much harder to start again. So much of the time that pile of cash sits there doing nothing, when it should have been helping to secure a future.

Financial fitness gurus

As ever with human behaviour, there’s no quick fix, no magic words to solve it. We like to think of ‘financial fitness’ in the same way as physical fitness. You need help to achieve results.

To get physically fit, you need a personal trainer. High-level athletes all have fitness coaches, and it’s not just to tell them what to do, it’s to help make sure they do it. Personal trainers do this in lots of different ways – whether it’s regular meetings, advice about diet, or simply encouragement and support.

Helping someone with their financial fitness is the same. Regular reviews, advice about saving and spending and encouragement and support are all part of this. It’s not about taking the lizard out of the equation – it’s about knowing how to offer support when the lizard is running riot. Helping someone to cage their lizard is an ongoing process, rather than a one off event.

We’re excited to announce that 7IM for Private Clients, London, has now merged with, and rebranded to, Amicus Wealth Management.

This marks a vital step forward in our mission to deliver the very best wealth management for our clients.

While our name has changed, our values and commitment remain the same. We’ll continue to provide personal, bespoke financial planning, built around you.

Explore Amicus Wealth Management