Federal Reserve Meeting

Framing is everything.

Compare the two sentences below:

‘The Federal Reserve raised interest rates by another 0.25% this week.’

‘The Federal Reserve raised interest rates by just 0.25% this week.’

Both accurately describe what happened, but the emphasis is completely different. The first version suggests that the pressure is still increasing, whereas the second suggests that the end is near.

In fact, following the meeting, the market moved to price in 0.5% of rate cuts by the end of 2023 – despite Jerome Powell explicitly saying, “I just don’t see us cutting rates this year”!

Fed Chair Jerome Powell may have meant the former, but financial markets have, so far, interpreted the move as the latter. In fact, following the meeting, the market moved to price in 0.5% of rate cuts by the end of 2023 – despite Jerome Powell explicitly saying, “I just don’t see us cutting rates this year”!

So, what to make of it all?

Well, firstly, we’re reminded of some excellent work by Empirical Research Partners. They dug into the data and looked at market reactions to Federal Reserve decisions. Going back 70 years, they found that two-thirds of the time, the initial market reaction to a change in interest rates was wrong on a 12-month view. So, if the market bounced on the day of the move, there was a 66% chance that in a year, the market would be down. And vice versa. If nothing else, that should give any investor caution in predicting where the market might be, based on immediate responses to monetary policy.

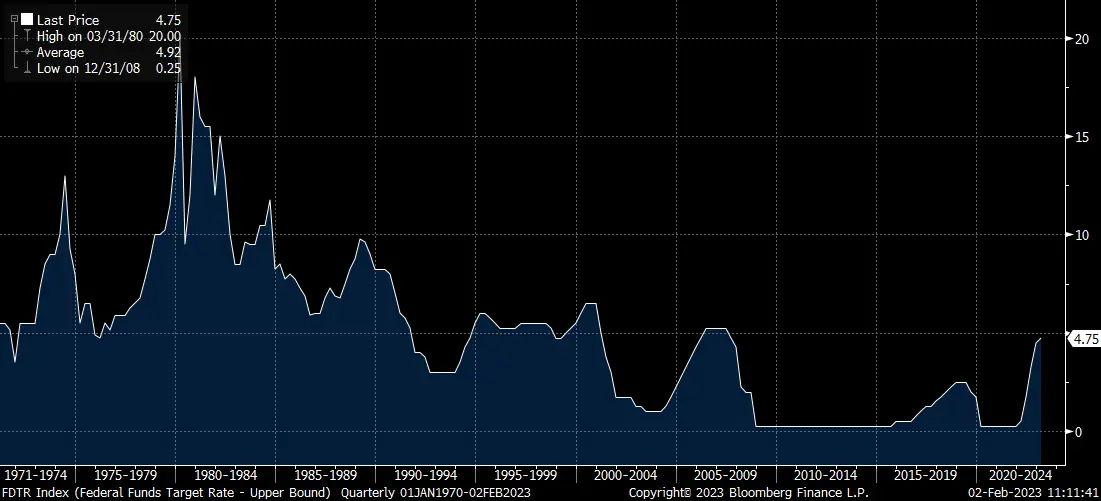

Secondly, we think that there’s a tendency for investors to believe that the path of interest rates will follow a predictable path. If you roll a ball on a flat surface, it starts off moving quickly, before slowing and then stopping, due to gravity and friction. And it’s tempting to apply the same kind of thinking to interest rate hikes; large ones first, then smaller ones, before they stop completely. But that’s not how it works. Just looking at a chart of Federal Reserve interest rates (below) suggests that there’s no smooth curve. There are pauses, and small cuts, and large cuts, and large hikes, and small hikes. As the Fed says, it’s ALL ABOUT THE DATA. And the same is true for the Bank of England and the European Central Bank, both of which raised rates this afternoon and suggested that more would come if needed.

Source: Bloomberg Finance L.P.

So, we prefer to think about the inputs the Federal Reserve is going to be monitoring over the next few quarters. And the outlook there doesn’t make us optimistic about the continuation of an equity market rally. Either inflation subsides due to a slump in growth (bad for earnings and share prices), or growth continues, which leads to sustained inflation, prompting further rate hikes (bad for share prices).

We’re still underweight equities – especially US mega-cap technology, preferring commodity producers and healthcare businesses. And we’ve been adding to government bonds over the last six months, in order to prepare portfolios for tough economic times. It can feel painful to miss out on these short and sharp rallies, but we believe that the conservative approach at the moment means focussing on protecting our clients’ capital ahead of a difficult economic period.

You can download the article as a PDF here.

We’re excited to announce that 7IM for Private Clients, London, has now merged with, and rebranded to, Amicus Wealth Management.

This marks a vital step forward in our mission to deliver the very best wealth management for our clients.

While our name has changed, our values and commitment remain the same. We’ll continue to provide personal, bespoke financial planning, built around you.

Explore Amicus Wealth Management