Monthly commentary

Portfolio Performance

At 7IM, we believe that taking a long-term view is essential when investing. We can’t always avoid the short-term bumps and shocks that the financial world has in store, but a well-diversified portfolio goes a long way towards smoothing out some of the journey. The long-term nature of our strategic and tactical process is a good complement to the Succession Matrix Expected Parameters.

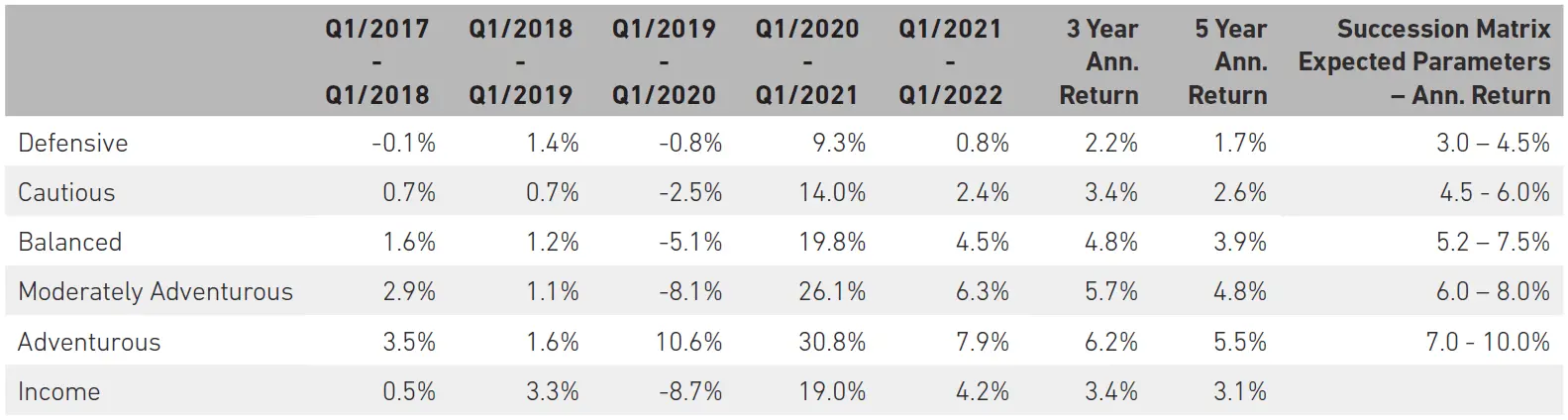

Source: 7IM/FE. Annualised return is defined as ‘Ann. Return’ in the performance table above and is as at end April 2022. The extreme COVID-19 related drawdown at the start of 2020 means performance should continue be viewed with caution. Portfolios are towards the lower end of their ranges for the five-year returns, with the more defensive end struggling a little in the face of low interest rates.

Market and Portfolio Review

After a difficult start to the year, April has been yet another brutal month for investors with Warren Buffet likening the stock market to a “gambling parlour” last weekend at Berkshire Hathaway’s annual conference. Most markets have been falling and a number of the classic ‘safe havens’ have not provided much shelter.

In terms of broad equity markets, the MSCI All Country World Index is down 8% for the month. US tech has been hit particularly hard as the Nasdaq is down 13% this month and a whopping 21% this year. Historically, investors have looked to fixed income to help out in sell-offs, but in this case, global government bonds have also suffered, slipping around 6% over the month.

Why have so many markets had such a hard time?

Different markets respond differently to global events, and there’s a lot going on at the moment. Let’s start with what’s happening in the world’s largest economy. US headline inflation is now at 8.5%, the highest it has been since 1981. The Fed are saying they’re serious about tackling it, and markets really do appear to believe them (at the moment). After May’s 0.5% hike, the market is pricing in another 0.5% hike at each of the next three Fed meetings – which would take the base rate to 2.75% by the end of 2022.

These two data points – US inflation and the Fed rate – can explain a lot:

Inflation is now high enough to panic equity markets; it has tipped beyond the point where planning investment decisions becomes difficult. This is one part of why stocks generally are sliding, but inflation can also explain why growth stocks are being hit hardest.

When inflation gets high, central banks tend to raise rates. Rising rates are worse for growth stocks as the high valuations growth stocks have demanded rely heavily on the prospect of strong future cash flows. The further in the future your cash flows are, the more rising interest rates will reduce how much those cash flows are worth to investors today. Instead, investors prefer to look for companies who are making money in the here and now – cash today is king!

Rising rates also explain the sell-off in bonds and the dollar rally. When US rates rise, money tends to flow to the dollar due to the increase in interest rates and returns available on dollar denominated assets.

Outside of the US, almost all other major markets have faced headwinds of their own:

There has been no conclusion to the Russia/Ukraine conflict and intensifying fighting has led to a further fall in confidence in European markets. As a result, MSCI Europe ex-UK is down 1.1% over the month.

In China, authorities are still taking extreme measures to battle covid outbreaks. Shanghai has spent the whole of April in heavily policed lockdown, and reports of Beijing going the same way have further dented sentiment. For now, the Chinese government is prioritising its zero-covid strategy over economic growth (although at the end of the month that focus may have shifted), and MSCI China has declined 4.1% in April as a result.

The UK has fared well as the FTSE All-Share is up 0.3% over the month due to certain characteristics of UK listed companies. Being a value index and having a considerable weight to commodities (especially oil) has really helped.

Where do we go from here?

Many investors’ portfolios will have lost money recently as the majority of asset classes have had a tough time, but there are lessons to be learnt:

Timing market drawdowns is extremely difficult. We have been saying that US tech is very expensive for a very long time. But knowing a market is expensive and knowing when it will take a haircut as a result of this are completely different. In recent months, sticking to our guns and being anti-fashion by being underweight US tech has paid off. Sometimes you really do have to wait for your views to play out.

Diversification is key. Harry Markowitz is reported to have said “diversification is the only free lunch” and recent drawdowns illustrate his point. Our equal weight bias has helped during this drawdown. A simple market cap weighting would have led investors to be overexposed to the growth stocks that have sold off most aggressively. When times get tough, it pays to have more thoughtful diversification.

Portfolio Positioning and Changes

During April, no changes were made to the Succession Model portfolios. They will be rebalanced in line with our quarterly schedule in May.

Core views

Growth will be stronger than the last decade:

Strong consumers, confident businesses and supportive governments mean one thing; stronger growth. The mushy, slow, volatile growth of the last decade will vanish, to be replaced with a more confident and self-sustaining growth cycle.

Inflation will be higher than the last decade:

The stronger demand does mean higher inflation too. To be sure, this does not mean worryingly high, but higher, nonetheless. This will have huge implications for interest rates and savers need to be ready.

7IM portfolios are positioned for the new cycle. We are:

- Positioned away from mega-cap US internet stocks and towards cyclical companies in developed markets, and high emerging market equity allocations.

- Underweight government bonds in a rising rate environment; seeking higher returns in specialist fixed income.

- Overweight alternatives to offer defensive qualities

- Longer-term investments in climate change and healthcare

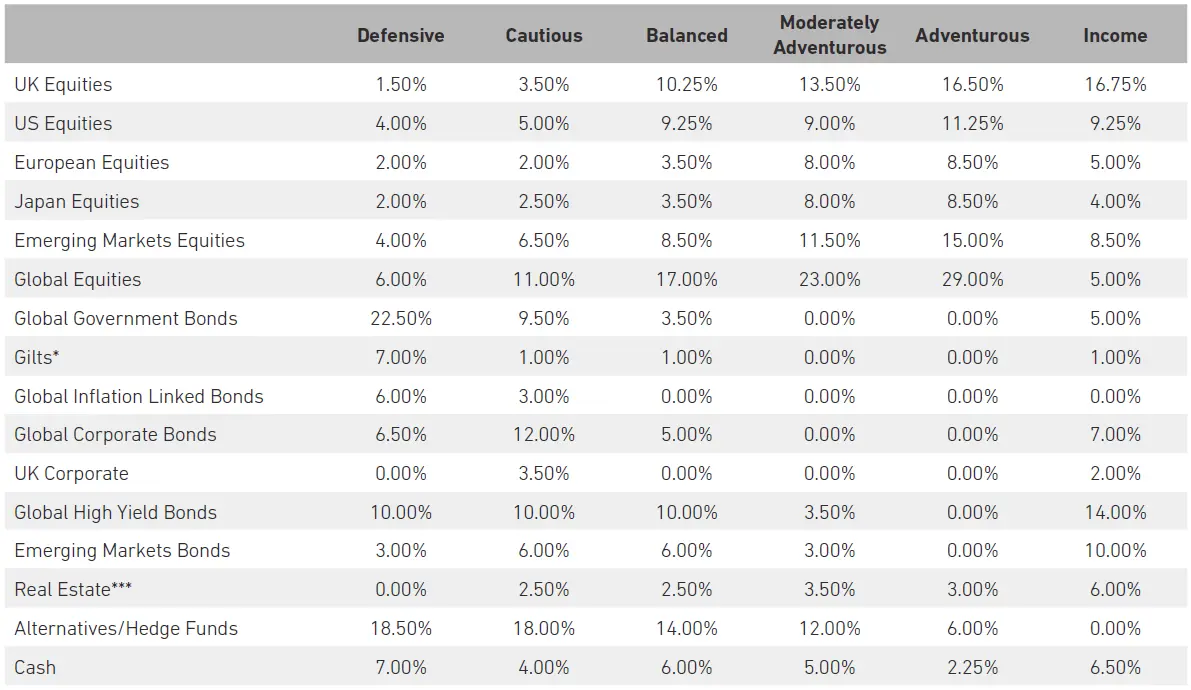

Detailed asset allocation

Source: 7IM. *Includes Short Term Sterling Bonds **Includes Convertible Bonds ***Includes Infrastructure

Read more from 7IM

You can download the commentary as a PDF here.