Monthly commentary

7IM’s thoughts on the Middle East

We know the footage of missiles streaking through the sky in the Middle East is alarming and concerning, especially as there’s no immediate suggestion that either side of the battle are going to step down. This is both a humanitarian and economic event, and our thoughts are with those affected.

We can’t give any assurances of how things will develop or how long this conflict will last. But what we can do is analyse how markets are reacting, digest the lessons from the past and evaluate portfolios to ensure we’re comfortable they remain appropriate to deliver on their long-term objectives.

Here we provide a brief summary of our initial thoughts and results of this analysis.

Portfolio exposures

A key consideration in constructing any investment portfolio is to ensure broad diversification of companies and asset classes. If done properly, it should provide a good level of resilience when market turbulence ensues. When we look at the 7IM portfolios, we see a well-diversified spread of assets, across companies, regions and sectors. In particular, the portfolios have near-zero direct equity and emerging market bond exposure to Iran or Israel. And the maximum equity exposure to the whole of the Middle East is 0.5% of portfolios.

How are markets reacting?

Markets are currently digesting developments in a measured fashion. Although they’ve moved lower, there’s not yet any signs of indiscriminate selling or panic.

At time of writing, the FTSE 100 Index is down around 4%, while the US equity markets have proven more resilient with only a 1.5% decline. To add some extra context, despite the past couple of days, the FTSE 100 is still up 5.6% for the year so far.

The big move we’ve seen since the strikes against Iran started at the end of February is in the oil price, which is up about 12%, as at time of writing.

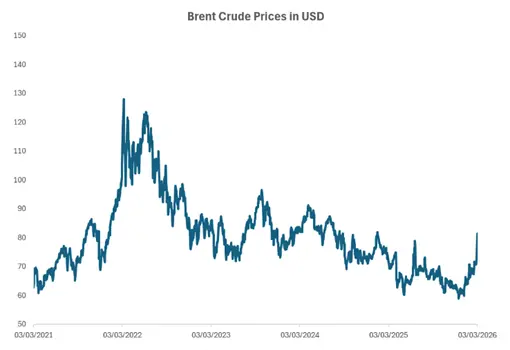

Why oil prices moved

Context is key here. The price of oil has been creeping up over the past six months, reflecting the risk that escalation with Iran could take place. Of relevant note is that four of the eight key shipping routes globally sit within the Middle East, with Iran controlling a key part (Strait of Hormuz). This explains part of the reaction we’re seeing, while future movements are uncertain, you’ll see this move just brings us back to average for the last five years:

Source: Bloomberg Finance L.P.

How we’re monitoring developments

A key watchpoint is the potential knock-on impact to inflation. If energy prices go higher and stay high, then inflation is expected to follow. That means government bonds might not provide the same protection as usual and central banks may not necessarily cut interest rates at the anticipated levels. That's part of the reason we choose to diversify our diversifiers, using alternative strategies in addition to bonds.

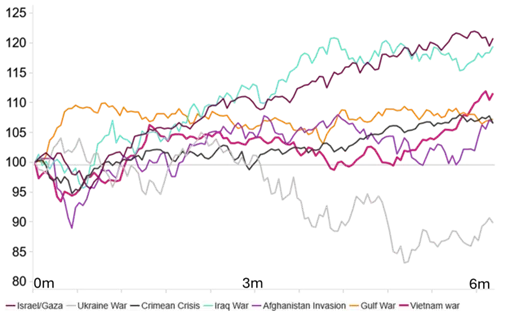

As you can see from the chart below, investors around the world are typically becoming accustomed to ignoring conflict as an impact on their portfolios.

There’s no reason in the immediate future to move portfolios in any way, but we’re continually monitoring the situation. More often than not, this is the right thing to do. As the chart shows, six months after the initiation of various conflicts, markets are usually back into positive territory.

Even in 2022, with the Ukraine war, the fall in markets was largely due to rising rates, rather than Russia.

Source: FactSet. Performance of the MSCI AC World in USD.

February markets wrap

Divergence was the name of the game in February, with global markets experiencing a strong month. Within equities, the US market lagged. Worries about how Artificial Intelligence might change unemployment levels – and hence, how much people spend -- continued to drag down the mood. One area hit particularly hard was software, as investors considered how AI could replace software packages. Software companies often set their fees by the number of users, so meaning that fewer employees would mean less revenue for software companies.

Outside the US, equity markets had a strong month.

- The UK was a standout performer, driven by lower inflation and the potential for a March rate cut.

- In Japan, positivity around the recently elected prime minister continues to push markets up.

Bond markets added some welcome stability. Global government bonds delivered positive returns across major developed markets. Part of this was due to anticipating falls in interest rates later in 2026. Corporate bonds also made gains, although riskier bonds struggled, particularly in the software sector.

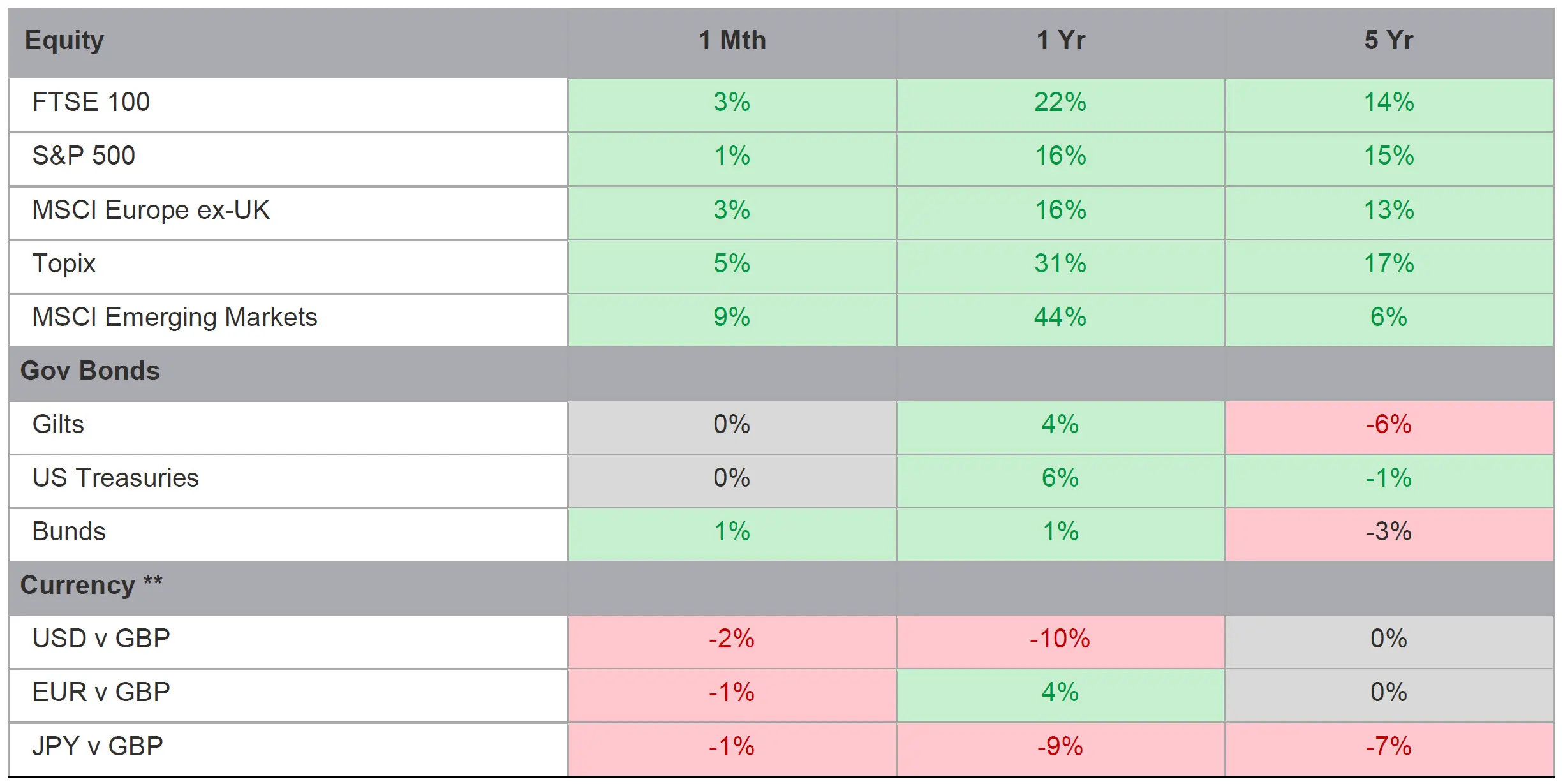

Market Movers

Quoted returns are in the local currency of the market

What we’re watching in March

- 17 March – US Federal Reserve meeting. Will Trump’s eagerness to have lower rates feed through to the voting committee?

- 19 March – Central Bank ‘Super Thursday’. A plethora of central banks will announce their views on interest rates, including the Bank of England.

More from 7IM