Monthly commentary

Portfolio Performance

At 7IM, we believe that taking a long-term view is essential when investing. We can’t always avoid the short-term bumps and shocks that the financial world has in store, but a well-diversified portfolio goes a long way towards smoothing out some of the journey. The long-term nature of our strategic and tactical process is a good complement to the Succession Matrix Expected Parameters.

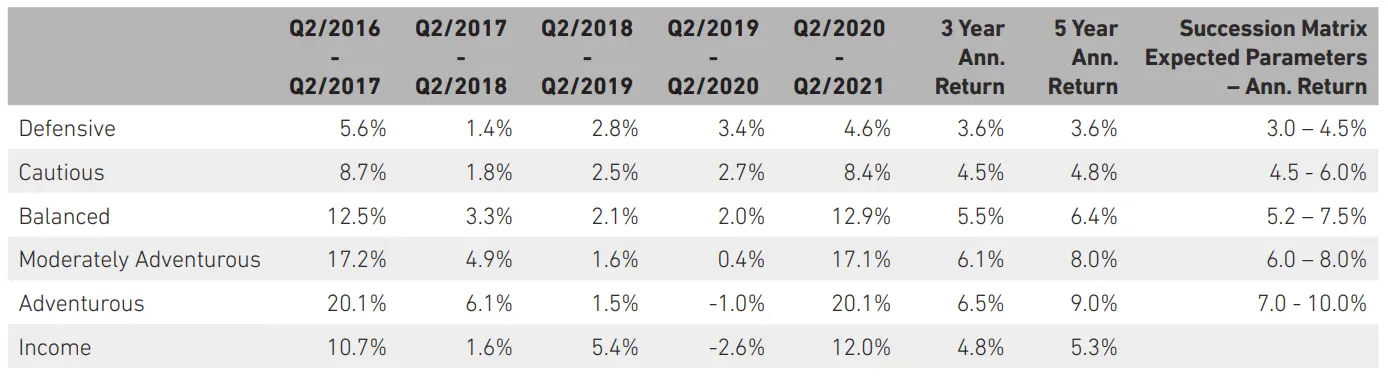

Source: 7IM/FE. Annualised return is defined as ‘Ann. Return’ in the performance table above and is as at end June 2021. The extreme COVID-19 related drawdown at the start of 2020 means performance should continue be viewed with caution. All portfolios are within their ranges for the five year returns, with the more defensive end showing particularly strong numbers.

Market and portfolio review

June has been somewhat of an emotional whirlwind in UK domestic politics. On 14 June, we found out that we would have to wait another four weeks for full post-lockdown freedom. Two days later, Dominic Cummings released WhatsApp conversations in which Boris Johnson branded Health Secretary Matt Hancock as hopeless. Always nice to know the boss has faith in you… And then, at the end of June, we saw Hancock’s resignation following some now infamous CCTV footage.

Outside of Westminster though, things are heading in a positive direction. It’s not just that football might actually be coming home, it’s that over 80 million COVID-19 vaccine doses have been administered so far, and the benefit of these will be felt more and more as widespread immunity sets in.

In the US, the main talking point was the Federal Reserve’s slightly confusing messaging. On Wednesday 16 June, the Federal Open Market Committee meeting hinted that unemployment would be transitory and inflation wouldn’t be, and so interest rates might need to rise ever so slightly more quickly than previously thought. But then, in his testimony to Congress the following Monday, the Fed Chair Jay Powell was much more dovish, suggesting that both unemployment and inflation would be transitory.

The fear generated by the first announcement prompted an S&P 500 sell off. Powell’s later statement then reassured everyone, and the S&P bounced back up to exactly where it was before the first announcement. Making moves and changing portfolios off the back of every little announcement and microsignal is not how we run money. Anyone trying to decipher short-term markets ends up flailing around and chasing their own tails. This episode demonstrated something vital for long-term investors like ourselves – the importance of not reacting. Most of the time, as the world returns to normal, the trick is to do nothing.

The numbers are staggeringly clear. The S&P 500 opened at 4245.6 on Wednesday 16, fell 2% to 4166.5 on Thursday 18, but then closed on Tuesday 22 after congress at 4246.4. Lots of selling and buying over the five business days to end up precisely where you started.

We believe that the world is poised for a period of strong growth and portfolios are positioned to take advantage of this. Central banks may feed us some confusing messages, but that’s actually quite a normal state of affairs as they try to work out what’s best for the economy. Rate rises are still some way off and our view on government bonds hasn’t changed, we still prefer to invest in alternatives which offer defensive qualities and inflation beating returns.

Portfolio positioning and changes

During June, no changes were made to the Succession model portfolios but they will be rebalanced in line with the quarterly process in August.

Core views

A new wave of economic growth… For the past decade or so, the virtuous circle of consumption and investment has just not been able to get going. The scars of the financial crisis were too deep – people bought less stuff while governments reined in spending. As a result, companies kept putting off investing in longer-term projects.

The 2020 recession hit the reset button. People are willing to spend again, while governments have ditched austerity. And so, companies are starting to invest for the future. We are now at the start of a sustained period of growth, fueled by confidence and expansion across all sectors of the global economy.

And a little inflation won’t hurt… Economists tend to dislike thinking about the psychology of inflation, but in a lot of ways, someone’s inflation expectations are a good proxy for their confidence levels. With the right amount of price and wage growth, people are encouraged to make life decisions which are positive for the economy. We haven’t heard the word “Goldilocks” for some years now, but there really is an amount of inflation which is just right to keep things humming.

7IM portfolios are positioned for a changing environment… For this coming growth phase, we believe a more selective exposure will be better than a large overweight to the broad equity market. A more robust consumer-driven cycle will see different winners emerge. Regions and industries which have struggled to attract investors over the past decade are better positioned to capitalize than the huge US tech giants (although there are lots of small US companies which will do well).

We’ve also made sure that our fixed income positioning isn’t unnecessarily exposed to rate rises, using allocations to alternatives and to non-mainstream asset classes.

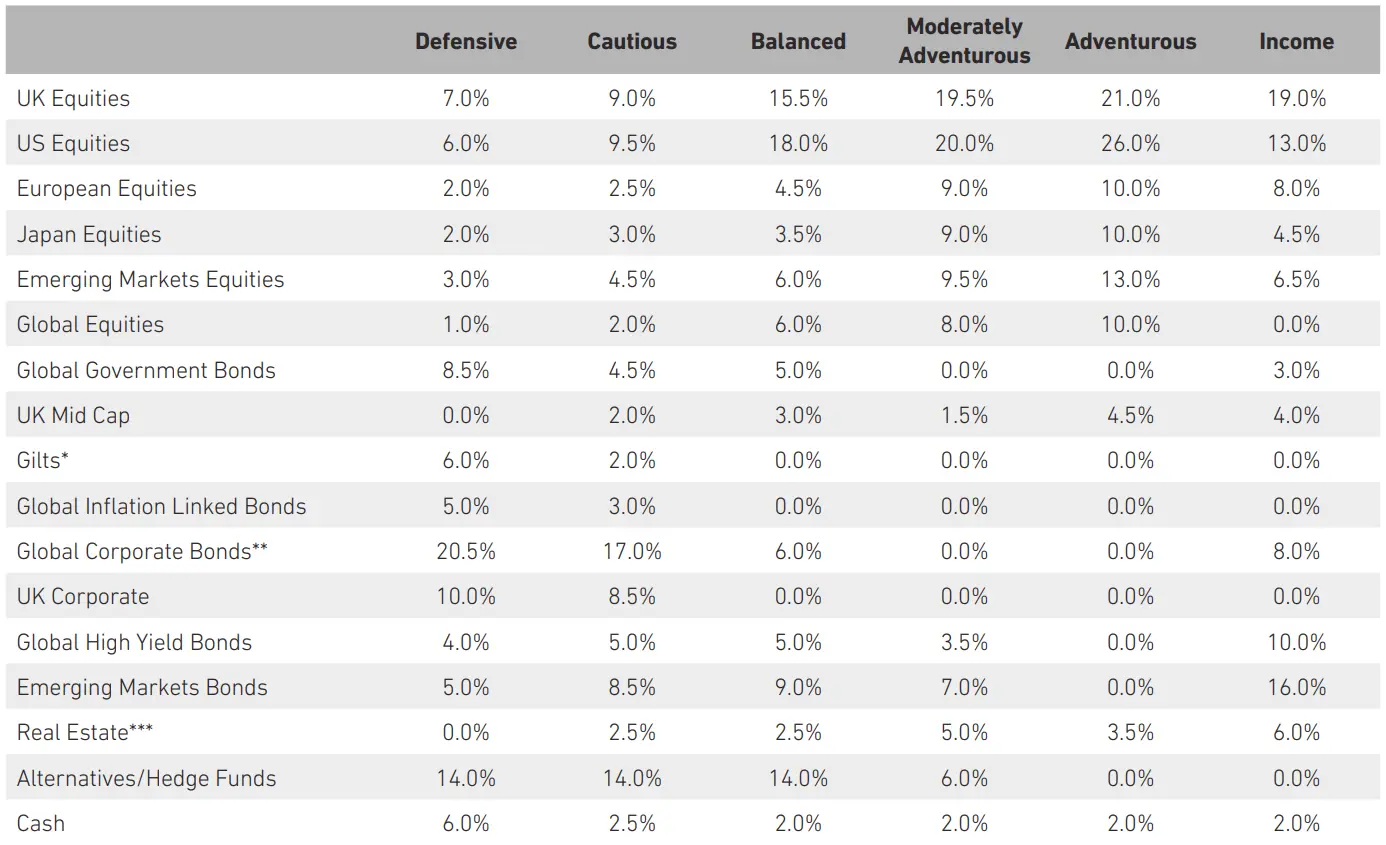

Detailed asset allocation

Source: 7IM. *Includes Short Term Sterling Bonds **Includes Convertible Bonds ***Includes Infrastructure

Read more from 7IM

7IM and Succession have come together to give your clients access to a range of risk-rated, low-cost model portfolios to help them achieve their goals.