Monthly commentary

Meet the new tech… same as the old tech

It’s 55 years (!) this month since The Who released Won’t Get Fooled Again*. At the end of the track, after Roger Daltrey’s iconic scream, he sings the line that sums up the whole track: “meet the new boss, same as the old boss”.

The month of May felt a bit like that for equity investors. Big tech came roaring back, with the NASDAQ up 11%. That was more than double the global equity market returns (a not too shabby 4.5%). It feels very familiar. You can make money in lots of places, but lots of money in one particular place…

And it prompts “new boss, same as the old boss” from two completely different types of investors.

The first – the “we’re so back” brigade – are the big tech believers: the same story of the past decade is playing out again. The gains will keep accruing to the biggest players; any new innovations outside of big tech will be bought or replicated or absorbed. Yes, there might be unheard of levels of spending on data centres ($700 billion estimated this year by the big five US tech companies), but all that means is they’ll be further ahead in a couple of years. Anyone who thinks the old way of investing is coming back doesn’t understand the future.

The second – the “oh not again” crew – are the opposite. They are seeing the final throes of last decade’s story. The big companies are too big, in competition with one another, and can’t keep growing sales at 20% per year. The amount they’re now spending, in areas where they’re inexperienced buyers (energy generation, power transmission, large-scale infrastructure) will come back to bite them. There might be a winner from the war for Artificial Intelligence (AI) dominance, but it’ll be a victory that costs the winner as much as the losers. Anyone who thinks the old way of investing is dead doesn’t understand history.

If you’re a record label, you have situations like this all the time. Should you take a risk on an old band with new songs? Or a new band with an established sound? Or something completely new and unknown? Can you get the music released in time to catch the current wave? Or are you creating a new one?

If you invest like we do, you don’t have that worry as much. We’re not in the position of a record label searching for the next hit. We’re on a long, long drive and trying to build a decent playlist with enough variety to last and enough familiarity to enjoy.

So yup, tech might still dominate. Technology is a big part of the world – and stock market! – so, it’s healthy to have a chunky allocation to tech stocks around the world. But equally, industrials and utilities might well benefit from the tech spending, so invest there too. And lots of other regions and sectors and approaches.

The best way to avoid a bad boss (old or new) is not to have a boss. We try to build portfolios that way.

*Probably my second favourite of theirs. I’ve been hooked by the Baba O’Riley intro since I first heard it. Other opinions are available.

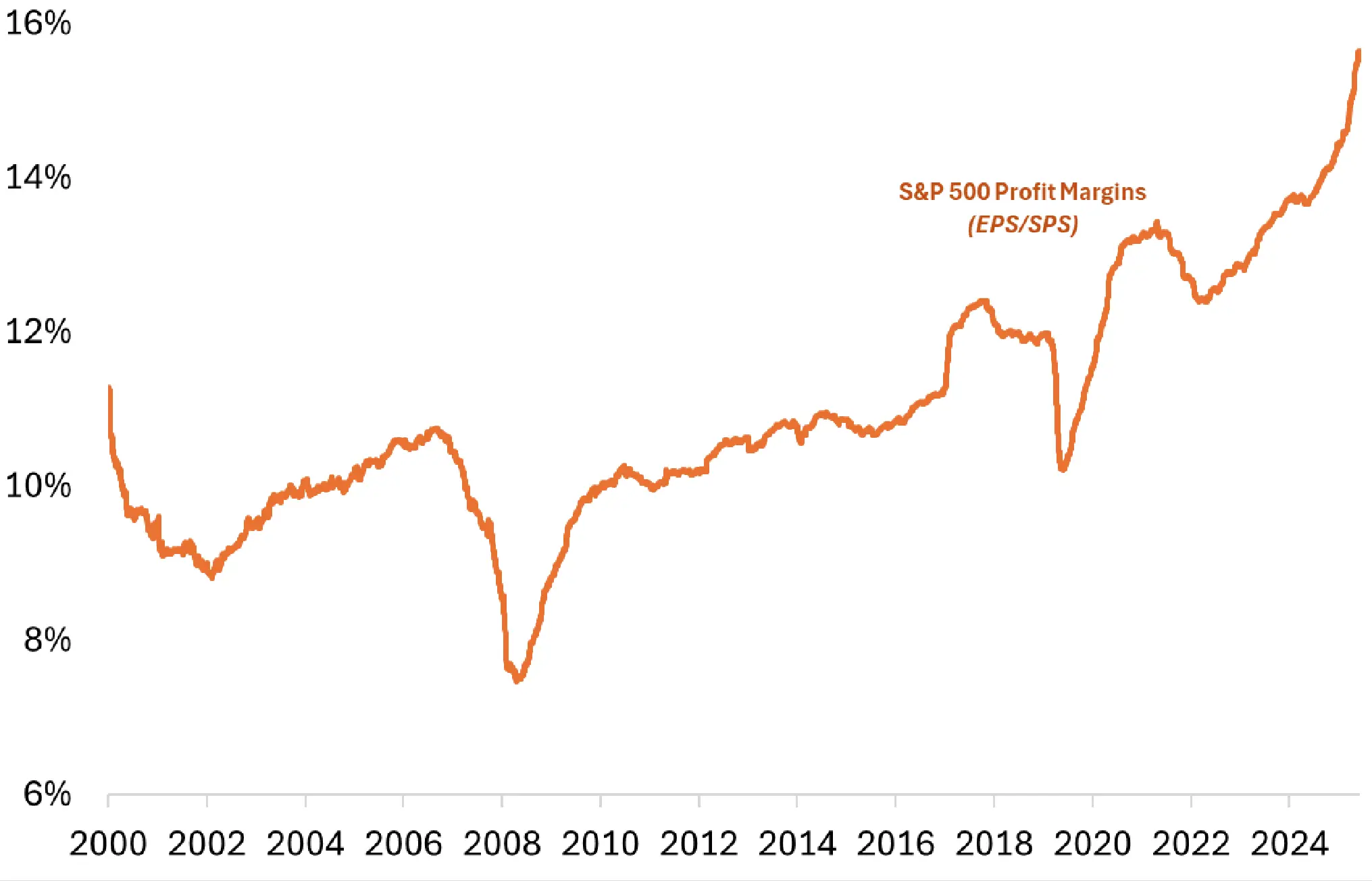

Chart of the month: US corporate profits keep growing

Stock market bulls will point to rapid corporate profit growth – especially in places like the US – as a sign that the market rally is not excessive. However, we think the data needs to be viewed a touch cynically.

The chart below shows the average profit margin for the S&P 500 Index, i.e. how much profit the average company is making for every dollar of stuff it sells. It ebbs and flows with economic cycles but has marched upwards from around 10% in 2005 to over 13% post-COVID.

Profit margins have risen sharply over the past two or three years. They now stand at 16% – almost a quarter higher than a few years ago.

Many will point to the rise of the big tech stocks, which have tended to earn fat margins. That certainly explains a lot of the rise over the last 15 years.

However, the recent spike appears more mechanical, a result of accounting treatment as much as true cash flow. The tech giants have ramped up capital expenditure (capex) on chips and servers. And that’s real spending. The suppliers – the contractors building the data servers, providing the trucks, the machinery, the "picks and shovels" – are recognising the capex boom as revenue today.

The strange thing is that for the spenders, most of the expense goes on the balance sheet, where it’s gradually depreciated via the income statement over several years. That means it only impacts profits a little bit each year, rather than all at once. The suppliers' profits are boosted instantly, but the hit to their customers' profits is delayed.

There's nothing nefarious about this – it's just an artefact of accounting – but it does raise questions about valuation multiples. At 7IM, we invest in the mega-cap giants and uncorrelated alternatives, which should help protect portfolios if markets prove frothier than at first glance.

Source: Factset/7IM

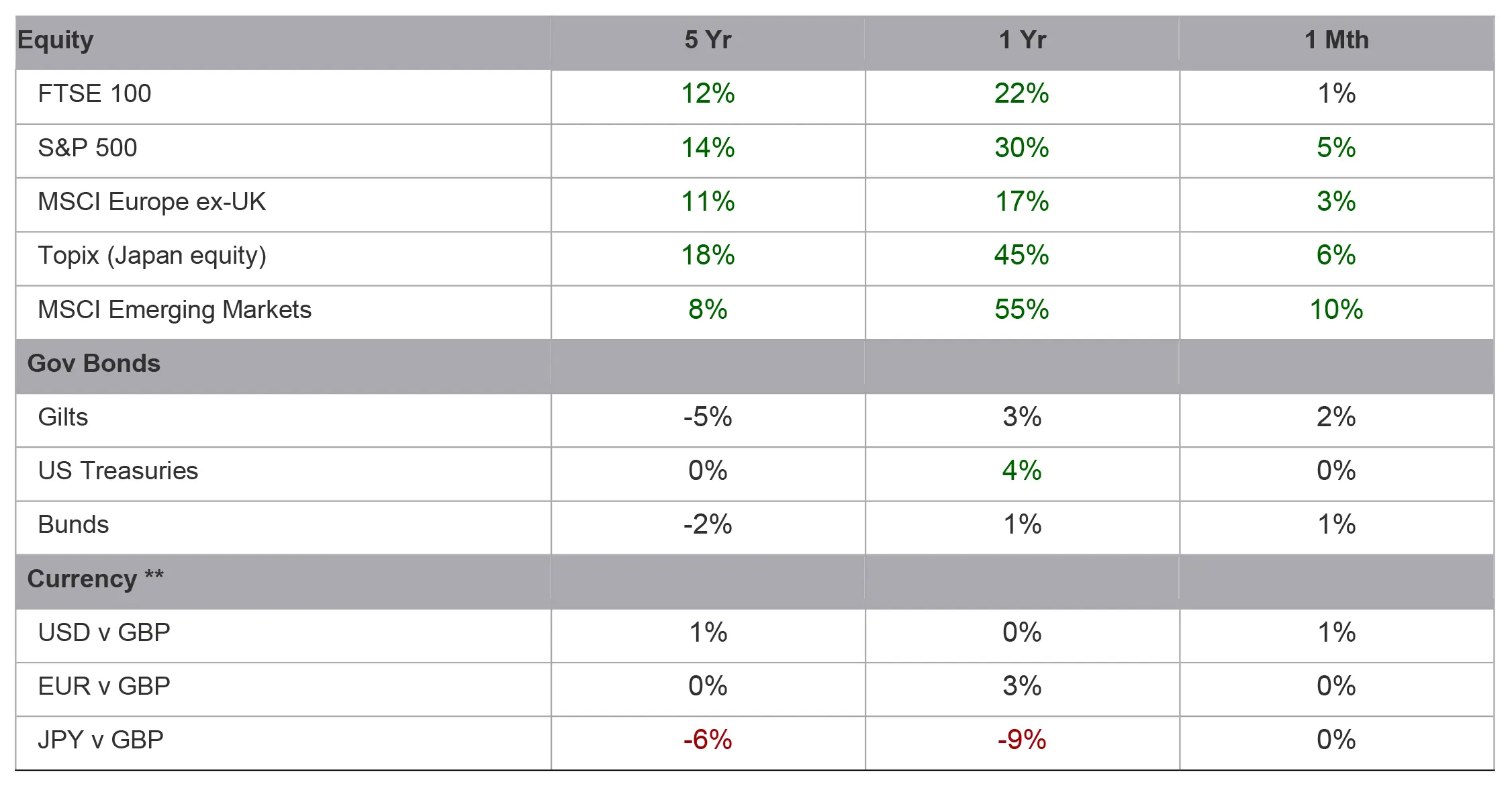

May markets wrap

The final days of May blanketed the UK in sweltering heat, and the red-hot global stock market was also busy hitting record highs.

The US market, which constitutes about two-thirds of the value of the global market, continued its march upwards, with the S&P 500 Index breaking the 7,500 mark for the first time. The rally was driven by a handful of big tech stocks, with Alphabet, Nvidia, and Apple all hitting record highs. Underlying the boom has been bumper corporate profits. Thanks to a combination of revenue growth, share buybacks, and margin expansion (see "chart of the month"), earnings-per-share have almost doubled since the start of the decade.

But America's performance pales in comparison to South Korea. The Kospi index rose 22% over May and has roughly tripled over the last year. Some of this is driven by genuinely exceptional profit growth, especially from chip giant SK Hynix (which rose a cool 81% in May), but there are also signs of a retail frenzy, with widespread reports of individuals using leverage to make bets on further price rises.

Things were calmer back in Europe, with French and German markets broadly unchanged over the month. The UK market was also flat, despite the oil giants like Shell falling as easing tensions in the Strait of Hormuz sent crude prices down.

By contrast, UK debt markets were in a rollercoaster. Gilts nosedived after the May local elections, as it looked like the Labour Party might replace Keir Starmer with a less market-friendly leader. The bond market tantrum sent long-term borrowing costs to their highest since 1998. The odds-on leadership contender Andy Burnham later backtracked on his more anti-bond market comments, allowing gilts to recover. Corporate credit spreads narrowed marginally, as easing geopolitical tensions fed into higher appetite for riskier bonds.

Market movers

Quoted returns are in GBP

What we’re watching in June

17 June – The US Federal Reserve has its first rate-setting committee since Kevin Warsh became chair. Fireworks are unlikely, but still worth watching!

19 June – The Makerfield by-election results. Will Prime Minister contender Andy Burnham get back into parliament? Gilt markets will be on high alert.

23 June – FedEx gives its quarterly earnings update; usually a good insight into global supply chains!

More from 7IM