Private credit 101

Before the Middle East crisis, private credit was worrying investors. And if things calm down, it may worry them again. Here, we’ll look at the sector. What is it? Why’s it making the news and should investors be concerned?

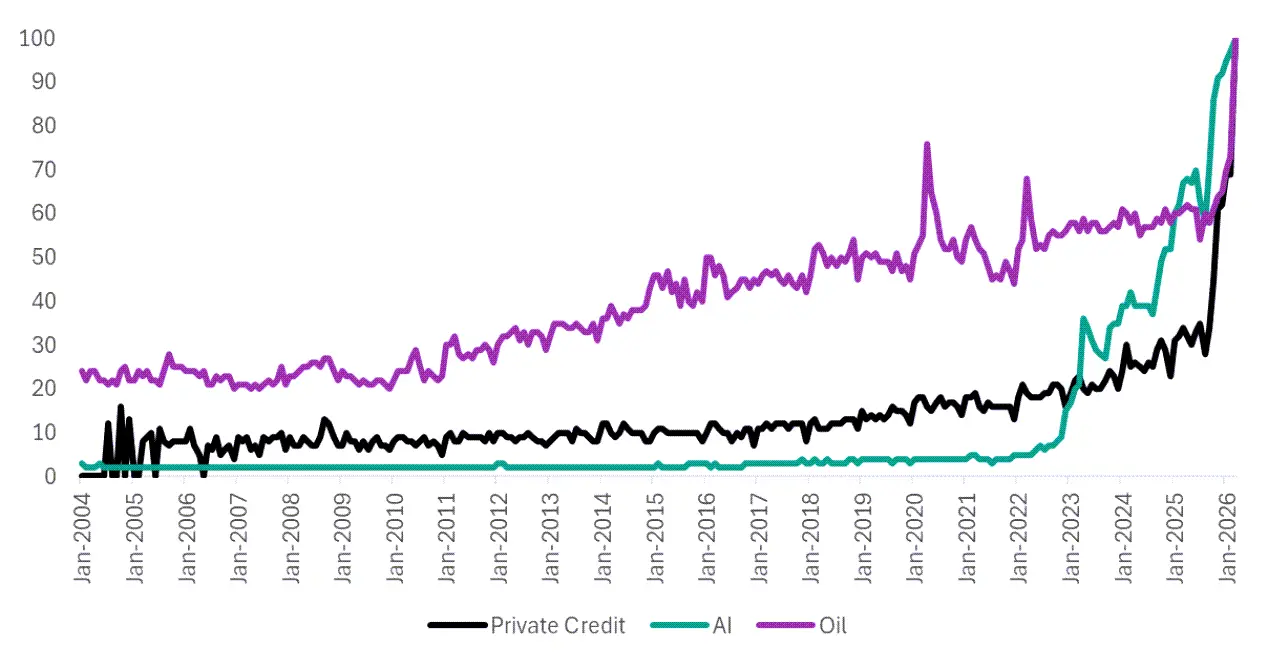

Google Trends: Private credit has been grabbing the news

Scale 0-100 with each search relative to itself

What is private credit? From clay tablets to spreadsheets

Credit is as old as civilisation. 4000 years ago, Ancient Egyptian merchants borrowed and lent. Instead of money on spreadsheets, it was grains tracked on clay tablets.

The tools have changed, but the deal hasn’t. One party needs money. Another wants a return. From London coffee houses to today’s global banks, it’s the same transaction.

Private credit is the same story. There are businesses who can’t (or won’t) borrow from a bank, and there are investors (insurers and pension funds) looking for a return. In between them are private credit funds, who do the credit work on the businesses, aligning loans with the risk tolerance of the investors.

“Private” means the loans are not traded like bonds. Each loan is negotiated one by one. Technically, you could still track on clay tablets.

Why is private credit ‘new’? Because something had to replace the banks

After the financial crisis in 2008, banks got told to stop lending quite so much.

Regulators worried banks had become too central to the global economy. So integral that if the banks don’t get paid back, a problem for the banks becomes a problem for us all.

So, regulators asked banks to hold more capital against riskier loans. Essentially, to make less money from lending. Keep lending to ‘safe’ larger companies, and not to ‘riskier’ smaller companies.1

That left private credit with a problem. Lots of the money that banks lent out came from people who were happy enough to put their money in the bank but wouldn’t dream of lending it to companies (even though it had been happening behind the scenes).

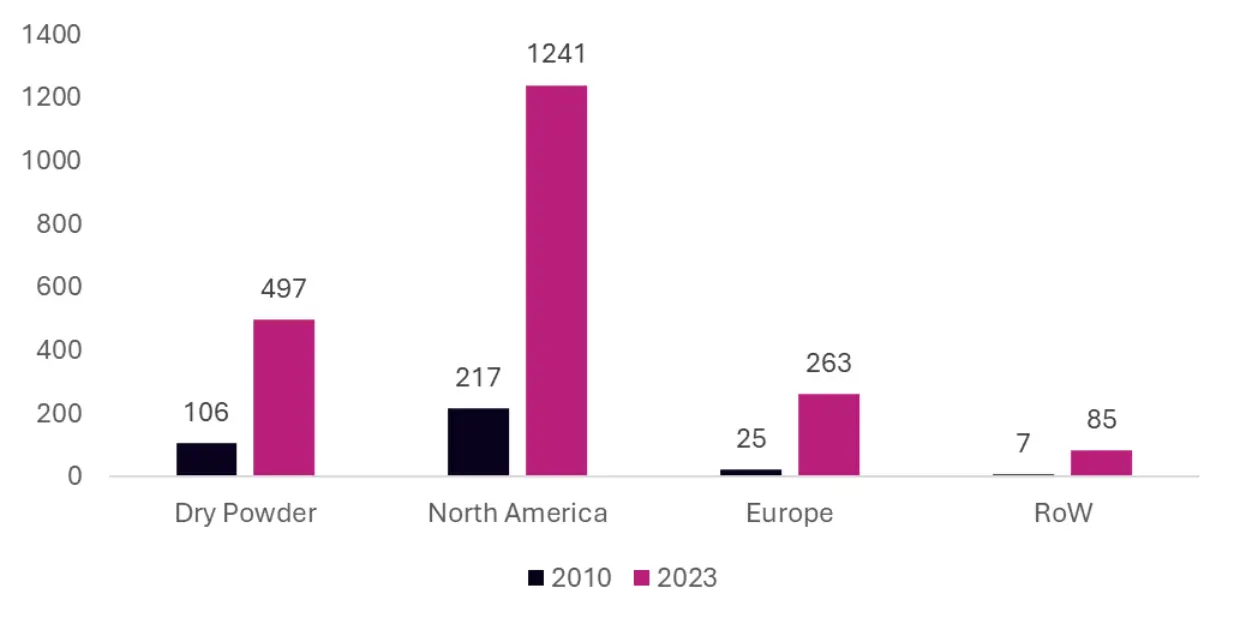

And with sensible risk provisioning and careful marketing, investors grew more comfortable. Evidently, because over the past decade or so, the private credit industry has grown to over $2 trillion.2

Funds managed by private credit outstanding

$ bil

Why’s it in the news? It was inevitable

An asset class doesn’t reach over $2 trillion by chance. Incentives lined up across the chain. Investors wanted diversification, and advisers wanted something different. Managers raised money to meet demand, while small businesses still needed capital. Falling rates added fuel, driving a search for yield.

Usually, funds would be closed-ended: find willing investors matching the investment horizon with the borrowing horizon of the business. No new shares issued, and you can’t get your money back until a specified time.

Investment locking isn’t for everyone. Evergreen funds changed that. They allow limited withdrawals, under set rules. This broadened the investor base and sped up growth.

But lending has a basic rule. If you mismatch time horizons, this can come back to bite. And this has made the news.3

Funds usually set withdrawal limits upfront. A common rule is 5% of assets per quarter, with the rest queued. In calm markets, few investors test this. When nerves rise, more than 5% want out at once. Funds then say, as promised, “Sorry, not yet.” Cue outrage. But is it a big problem, or something more contained?

Don’t compare it to 2008

The media often reaches for the 2008 analogies. But this is NOT the financial crisis. Banks today are safer. They lend more cautiously and hold more capital. That makes them a stronger buffer for the system.

What this means for investors

A more useful comparison might be US shale energy in the mid-2010s. Smaller firms borrowed heavily to fund growth, often with weak cash flow behind it.

When oil prices collapsed in 2014, defaults rose and parts of the market sold off. It was uncomfortable, and some investors lost money. But the wider market was unaffected.

With private credit, we expect pockets of strain. Small software companies look under pressure. Some private credit funds might face stress. Some investors may take losses.

This is part of the ebb and flow of financial markets. Risky lending should have some defaults… that’s the “risk”!

It’s the same story we’ve seen for 4,000 years. An Egyptian merchant on the hook for a specific grain shipment might fail to pay his loan back. But overall, lending and borrowing kept going – creating massive wealth. The system survived and thrived. The pyramids are still standing.

1 https://www.bis.org/publ/qtrpdf/r_qt2503b.htm

2 https://www.moodys.com/web/en/us/insights/podcasts/inside-economics/private-credit-systemic-risk.html

3 https://www.nber.org/system/files/working_papers/w6906/w6906.pdf

More from 7IM