Quarterly Rebalance Commentary

Overview

The last three months have seen a shift in the market perception of what’s important, with some of the trends from last year turned on their heads. Before Christmas, the world was worried mainly about the Omicron variant of COVID-19. Once the New Year began though, focus has moved to the outlook for interest rates and inflation, with a smattering of geopolitical tensions too.

In terms of market performance, we’ve seen large US tech companies lose their halo of invincibility, and investors shifting towards more cyclical parts of the equity universe; energy companies, banks and non-US markets. These are the types of shift we’ve been expecting for a while now, and we believe they’ll continue.

Core investment views

Growth will be stronger than the last decade: The mushy, slow, volatile growth of the last decade will vanish, to be replaced with a more confident and self-sustaining growth cycle. There are three key drivers of this:

- Consumer demand… The COVID recession has left consumers in the US, and the rest of the world, with a lot of cash. When they have cash, they tend to do one thing… spend!

- Governments have abandoned austerity… governments are biased towards spending, rather than cost-cutting. Large-scale government projects create lots of demand, and lots of jobs.

- Businesses are more confident… there’s nothing business love more than cash-rich consumers and investment-focused governments. With demand rising, CEO’s start thinking about investing in growing their productive capacity and their workforce.

Inflation will be higher than the last decade: The stronger demand does mean higher inflation too. To clarify, this does not mean worryingly high, but higher, nonetheless. Once we move past the COVID-19 supply chain spikes, we’re likely to enter an environment where inflation is above the 2% bank target for a number of years.

Inflation is a driver of economic expansion – more so when it’s positive than when it’s at zero, or negative. Look at Japan for a clear example of what can happen to an economy when inflation goes missing for a few decades!

However, this will have huge implications for interest rates and savers need to be ready. 7IM portfolios are positioned for a changing environment…

7IM portfolios are ready for the new cycle:

- Positioned away from mega-cap US internet stocks; favouring cyclical companies in developed markets, and high emerging market equity allocations.

- Underweight government bonds in a rising rate environment; seeking higher returns in specialist fixed income.

- Overweight alternatives to offer defensive qualities.

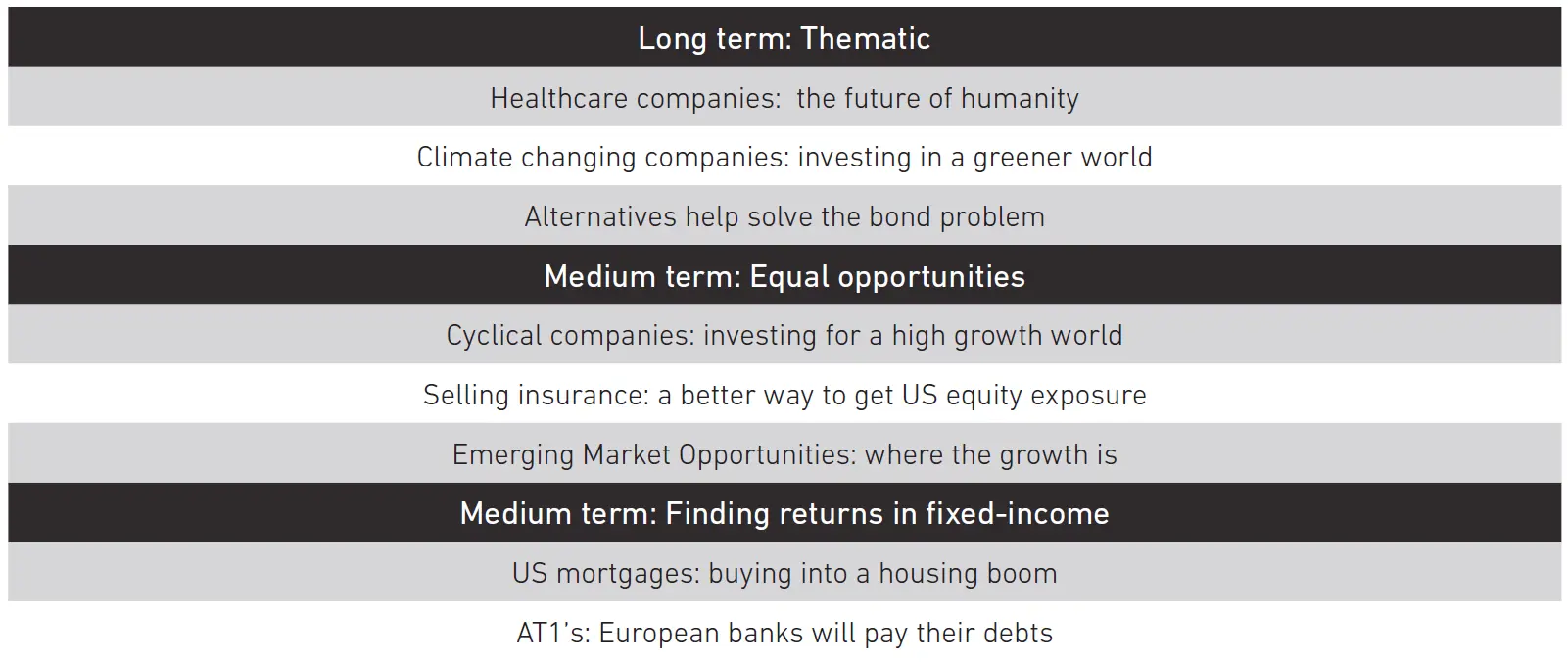

- Longer-term investments in climate change and healthcare.

Asset allocation changes

We made only one significant asset allocation change this quarter – selling our Asian high yield position to invest in the emerging market (EM) equity index. Both Asia high yield and EM equities had a tough 2021, but we view the potential for a strong bounce-back as greater in the equity space.

Chinese policy is tilting towards easing as President Xi looks to boost growth – usually a positive for Chinese companies, but also broader global growth. At the same time, EM equity valuations are the cheapest they’ve been since the early 2000s (the last time we saw significant outperformance!). EM currencies tell a similar story – as cheap as they’ve been since the early 2000s. We believe that the growth impulse combined with these starting valuations make EM equities extremely attractive at this point.

Manager updates

We introduced three new holdings across our range this quarter:

Baillie Gifford Health Innovation. This fund is our way of enhancing our exposure in our healthcare theme for higher risk profiles. We’ve added this as a way to benefit from a more discerning approach to buying stocks in this highly innovative part of the global equity markets.

ASI Global Inflation-Linked Bond Tracker. This is a much cheaper way to allocate to inflation-linked bonds than other passive options available in the market.

Invesco MSCI USA ESG Universal Screened UCITS ETF (GBP-hedged). This vehicle helps to move portfolios closer to our decarbonisation targets by screening out the more egregious polluters from the US equity market. It is provided on a GBP hedged basis which also helps manage currency exposure for our portfolios.

Please note: All of the comments in this document refer to the models we run on the 7IM platform, but the models are also available on a range of other platforms. As much as possible, we try to replicate the models we run of the 7IM platform across all platforms, but due to differing security availability, not all of the points outlined in this document may be relevant across these platforms. If you are unsure whether certain changes apply to models on a specific platform, please reach out to a member of the team.

The past performance of investments is not a guide to future performance. The value of investments can go down as well as up and you may get back less than you originally invested. Any reference to specific investments are included for information purposes only and are not intended to provide stock recommendation or investment recommendations to individual investors.

Read more from 7IM