Monthly commentary

Forget the Strait of Hormuz.

Just for a bit.

Not because it isn’t important, but because right now, financial markets are acting like it isn’t.

There’s a great meme going around my nerdy finance circle saying “EBITDA = Earnings Before Iran, Tariffs, and Donald Announcements”. And for most of April, that appears to be exactly what investors have focused on, as companies line up to report their Q1 results.

Searching through the transcripts of earnings calls, pretty much every CEO has paid lip service to Iran or oil in some way, shape or form. Always nice to have a scapegoat to blame something on, just in case. But this quarter, the goat seems healthy.

In the US, profits have grown by close to 25% compared to 2025; the last time we saw figures like that was during the bounce back from COVID. And although big tech is doing a lot of the heavy lifting, only around a tenth of US companies have failed to beat estimates. So, it’s not a case of winners and losers, more like large winners and small winners. Everyone gets a medal.

One of the fundamental rules of the twentieth – and now twenty-first – century is still in play. “When you’re smiling … the whole world smiles with you.” It’s just as true about America today as when Nat King Cole sang it in the 1950s.

If the US can grow, the rest of the world gets carried along.

If Amazon or Microsoft or Alphabet are going to put data centres in Europe, that boosts the local economy. If US industrial companies are churning out goods, they need the raw materials from everywhere else. And if US consumers keep spending, that money makes its way around the world.

Of course, it’s worth watching things like the petrol gasoline price in the US – around $3.50 per gallon before Iran, now up to $4.80 per gallon. The average US consumer still runs their life on gasoline, so prolonged pain here will eventually take its toll.

But (to bring Hormuz back in), that’s possibly the sort of widespread issue which prompts a speedy resolution. Without $6 gas, we don’t get back to $3 gas.

In the meantime, America is still smiling. And therefore, so are we.

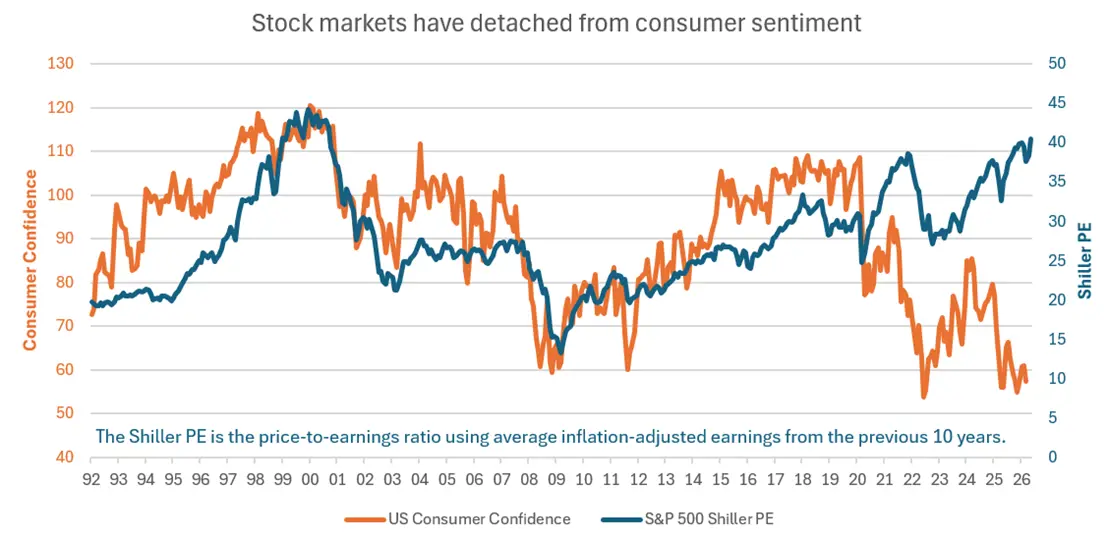

Chart of the month: Highs and lows

Stock market valuations used to move (roughly) in line with consumer confidence. The two reinforced each other, with bullish consumers fuelling earnings growth and bidding up stocks, while higher stock prices made consumers feel richer. This was true using US data (as shown here) and in other countries too.

But in 2020 the relationship broke down. Both dropped during the COVID pandemic, but stocks quickly rebounded to new highs, while consumer confidence never recovered. Both fell again in the inflation wave of 2022, and again stocks rebounded while confidence stayed even further down.

On the latest reading, confidence is below 2008 levels – it’s quite a feat to be more economically miserable than during a banking collapse – while stocks are bubbling along near record highs. What gives?

From the corporate side of things, it’s as simple as profits. US companies are turning sales into profits at the most efficient rate in the last century (they’re smiling).

The confidence aspect is perhaps more about society; it seems as if there’s more bad news than ever floating around – more outrage over the price of eggs, or student loans, or politics.

So, there’s a strange psychological separation taking place. Ask someone about their portfolio, and they can tell you the good things. Ask them about the world and they’ll focus on the bad…

Source: BEA/7IM

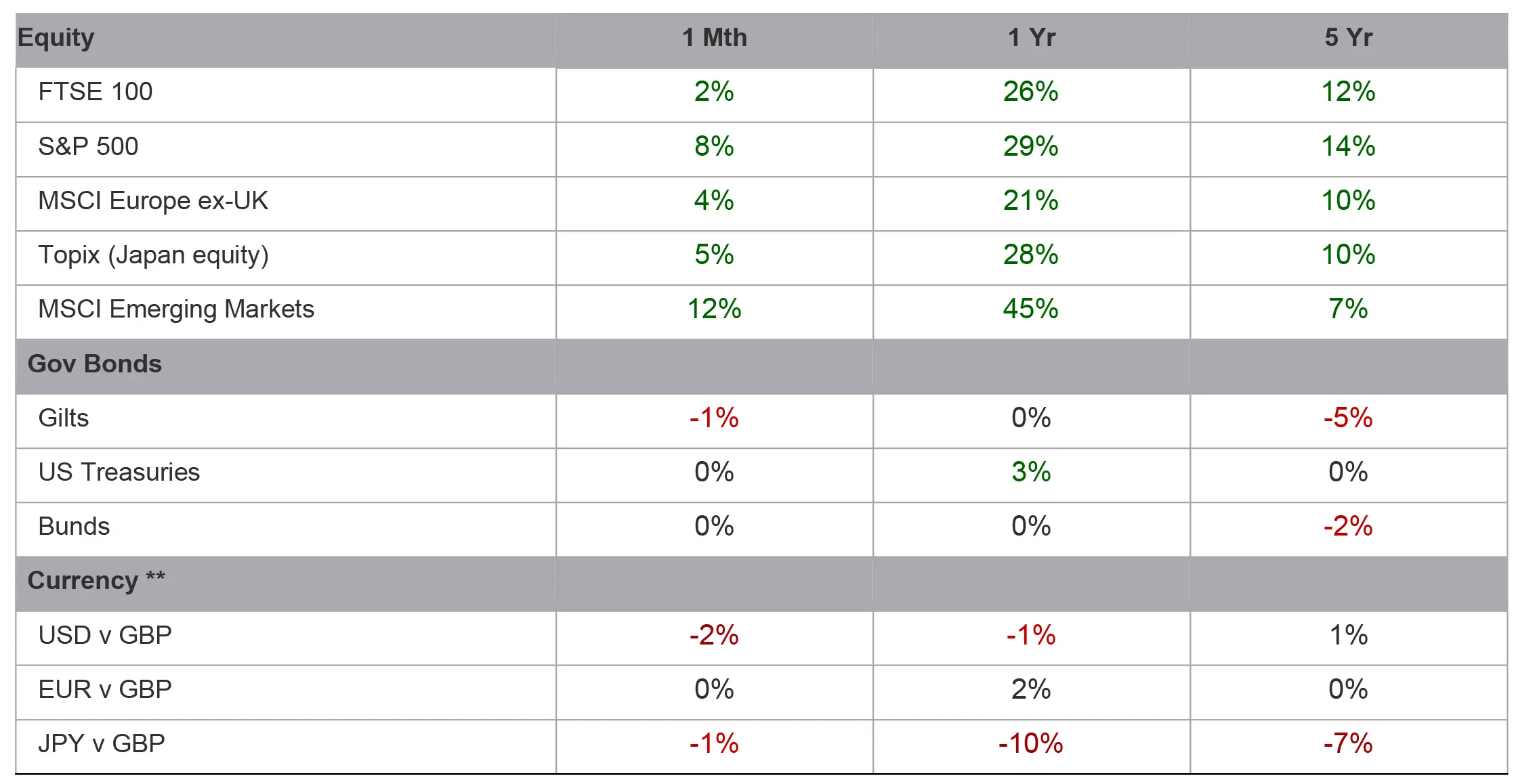

April markets wrap

Stock markets delivered a joyless rally over April, driven by a shaky ceasefire in the Middle East. Vast flows of crude oil, jet fuel, refined petroleum, fertiliser, sulphur, and helium (vital for making AI chips) remain offline, but markets are betting they’ll resume sooner rather than later. Meanwhile, stocks got a boost from blockbuster earnings reports from the big companies leading the way on artificial intelligence. America's S&P 500 Index logged its biggest monthly gain since the vaccine bounce in late-2020.

The UK market was more lukewarm, partly because of its large weights to crisis-beneficiaries like oil giants and weapons manufacturers. These rallied on the outbreak in March but plateaued on the de-escalation. A similar dynamic was at play in Europe.

The core locomotive behind the global rally was the technology sector. The companies' large future cash flows make them a prime beneficiary of lower inflation expectations. Plus, a raft of Silicon Valley giants released red-hot Q1 earnings. Alphabet, Amazon, Meta and Microsoft all beat earnings expectations. Alphabet stood out, reporting an 81% rise in profit as AI lifted revenue, sending its valuation surging to over £3 trillion.

The tech boom isn’t entirely limited to the US. In South Korea, Samsung shares rocketed 32% over April. The smartphone giant makes up about one-third of Seoul's stock market, propelling the country index –and the wider Asian market higher.

Bonds were mostly flat-to-positive, as inflation expectations drifted down on the ceasefire. However, gilts fell as markets priced in a “Rayner risk premium” amid concerns that Keir Starmer’s leadership looked wobbly. Gold also fell as emerging market governments, which had been prolific buyers, redirected their efforts to mitigating the oil shock.

Market movers

Quoted returns are in GBP

What we’re watching in May

8 May: if Labour gets a bad result from the previous day's elections, we could see a leadership shake-up with potential impacts on gilt yields.

11 May: the end of the core US Q1 earnings season, by which time we should know better if strong profit forecasts have held true.

15 May: Jay Powell's term as Fed chair ends, with Kevin Warsh expected to take the reins. Markets will be hanging onto Warsh's every word for clues as to the direction of monetary policy in the world's largest economy.

20 May: next UK inflation data release, which should give a clearer picture of how the Iran war has affected prices.

More from 7IM

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.