Quarterly Rebalance Commentary

Overview

Since our last model portfolio rebalance in February, a lot has happened. Markets were already moving downwards, and Russia’s move into Ukraine added to growing negative sentiment. A combination of negative sentiment, rising rates, and higher-than-expected inflation have meant that most equity and bond markets have suffered.

The MSCI All Country World Index is down 16% year to date. US tech has been hit particularly hard, as the Nasdaq is down 24% since the start of the year. Historically, investors have looked to fixed income to help out in sell-offs, but in this case, global government bonds have also suffered, slipping around 7% over the same timeframe.

Harry Markowitz is reported to have said “diversification is the only free lunch” and recent drawdowns really highlight this. Our equal-weight bias has helped during this drawdown. A simple market cap weighting would have led investors to be overexposed to the growth stocks that have sold off most aggressively. When times get tough, it pays to have more thoughtful diversification. Our alternatives allocation adds another layer to this and is outperforming broad equity and fixed income markets this year.

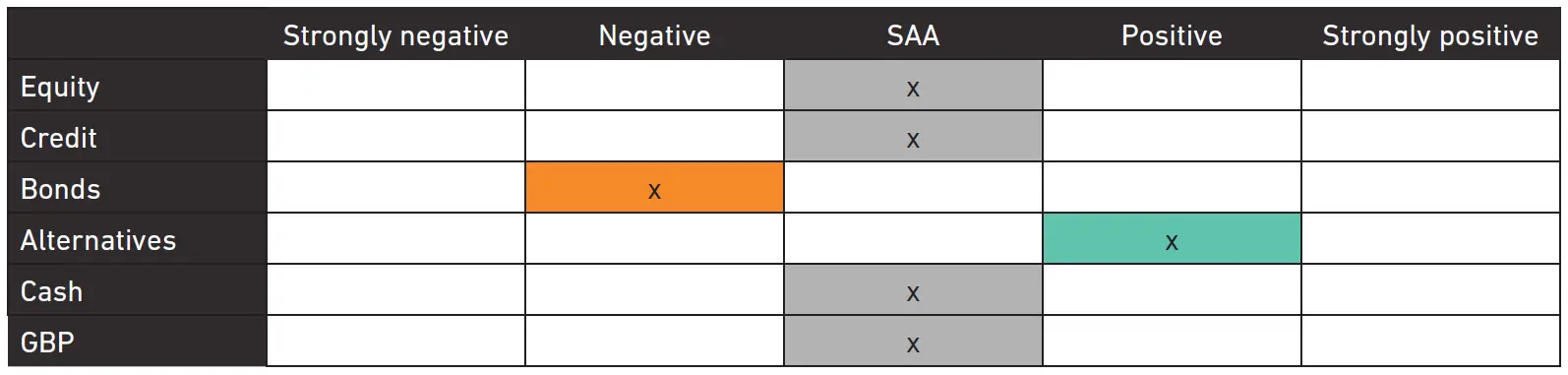

Despite global events, our portfolios have not changed much. Prior to the invasion, we were positioned for a higher inflation world, cutting back on our equity overweight, and favouring alternatives over bonds. This is why we don’t need to change portfolios much – we are well positioned for the world we are in and the world described in our core investment views.

Core investment views

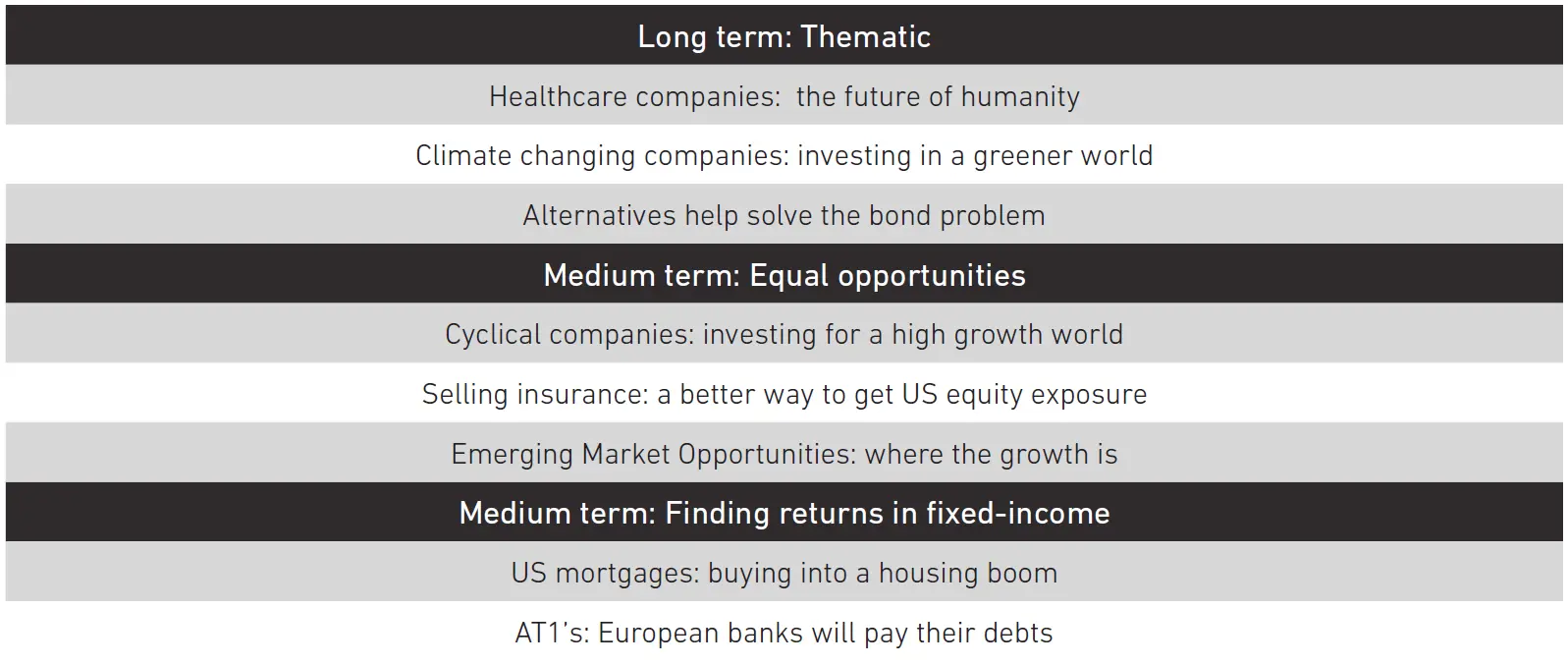

Growth will be stronger than the last decade: Strong consumers, confident businesses and supportive governments mean one thing; stronger growth. The mushy, slow, volatile growth of the last decade is no longer with us. The recent crisis in Ukraine takes the gloss off this a little, as Europe will take longer to get going. But Ukraine won’t stop a more confident and self-sustaining growth cycle in the US taking hold over the next 3-5 years – and nor will it impact the Chinese economic rebound.

Inflation will be higher than the last decade: The stronger demand does mean higher inflation. The recent shock to commodity prices only reinforces the view that higher inflation is here to stay. Over the medium term, we don’t believe that double-digit inflation will become embedded, but even 2-4% levels of inflation will have big implications for interest rates.

7IM portfolios are diversified and robust to geopolitical shocks:

- Global equity exposure is tilted away from expensive companies.

- Underweight government bonds in a rising rate environment.

- Overweight alternatives to offer defensive qualities.

- Longer-term investments in climate change and healthcare.

Asset allocation changes

The headline beta and duration exposures of our portfolios have not changed this quarter. We were well positioned to transition into the economic conditions we are currently experiencing.

We have, however, made some minor changes to our cyclical trade. We have sold out of the part of our cyclical basket that was in global mid-caps. This is due to a deterioration of the outlook for mid-caps generally. Mid-cap indices tend to have significant overweights to Europe, and a lot of these stocks have been shown to be quite sensitive to events in Ukraine. We would prefer to minimise our risk to the Russia Ukraine conflict as second guessing what will happen next is extremely difficult. The cash freed up by this decision was recycled into our SAA global equity allocation. We have maintained our Cyclical Champions theme through our global value position.

Manager updates

This quarter we have introduced the Fulcrum Diversified Core Absolute Return Fund to our alternatives basket to further enhance the diversification properties for this part of our portfolios. The fund is a combination of multiple alternative building blocks together in a single holding. Together it is taking many of the individually attractive and available strategies from the Fulcrum stable and combining them into one product. In particular, this includes allocations to equity dispersion and trend following strategies that we consider very attractive at this point in the cycle.

Please note: All of the comments in this document refer to the models we run on the 7IM platform, but the models are also available on a range of other platforms. As much as possible, we try to replicate the models we run of the 7IM platform across all platforms, but due to differing security availability, not all of the points outlined in this document may be relevant across these platforms. If you are unsure whether certain changes apply to models on a specific platform, please reach out to a member of the team.

Read more from 7IM

You can download the commentary as a PDF here.